- About half (51%) of the plans* it administers have adopted an auto-enrollment feature, a 28% increase since 2011.

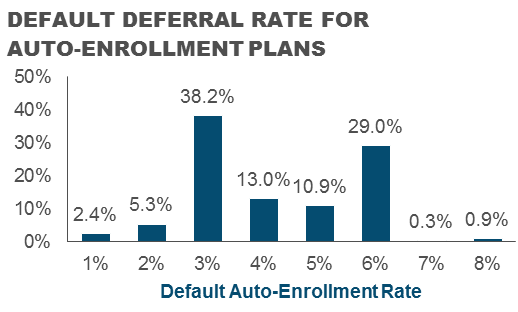

- 30% of plans have auto-enrolled participants at 6% or more, compared with just 17% in 2011.

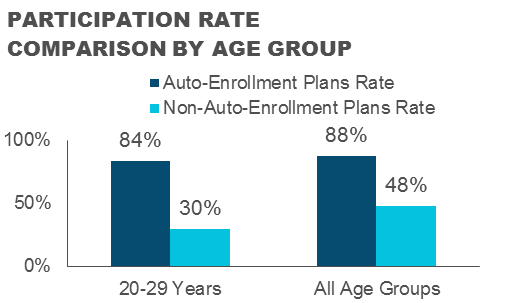

- Participation rates continue to be strongly tied to the adoption of auto-enrollment. Plans with an auto-enrollment feature have a participation rate of 88%, while those that do not have this feature have a participation rate of just 48%.

- Target-date investments continue to be the default of choice for 96% of plan sponsors.

CONTRIBUTION TRENDS: HALF OF PLANS NOW OFFER ROTH OPTION

By the end of 2015, half of the 401(k) plans recordkept by T. Rowe Price were offering their participants the option to make Roth contributions, an increase of nearly 49% since 2011. In addition, Roth contributions among participants increased for the eighth consecutive year. Regarding employer matching contributions, 40% of plan sponsors are now matching at a threshold of 6%.

But it’s not all good news. Among T. Rowe Price plan participants, the average deferral rate held steady at 7%, far below the recommended level of 15% that includes the employer match. In addition, approximately one-third of participants are not deferring any money to their retirement account.

GENERATIONAL FINDINGS: YOUNGER PLAN PARTICIPANTS INVEST IN TARGET-DATE FUNDS

While all generations will benefit from plan design features such as auto-enrollment, guidance, and participant engagement, generational differences often exist when it comes to saving behaviors and attitudes that plan sponsors should consider. Of the T. Rowe Price plan participant base:

- Younger participants (between 20 and 29 years of age) have a wider gap in participation rates when auto-enrolled (84%) versus not auto-enrolled (30%) than all age groups.

- Younger participants are also more likely to be invested in target date funds (70%) than other age groups (36%).

- Younger participants have a savings rate of 5%, considerably lower than older generations (between 7-10%).

- Participant guidance is also needed at the Gen X level, as the 40-59 and 50-59 age groups continue to maintain the highest outstanding loan balances, which has increased each of the past two years.

INDUSTRY TRENDS: MANUFACTURING INDUSTRY LEADING IN ADOPTION OF AUTO-INCREASE

T. Rowe Price clients receive access to a more in-depth view of select industries so they can compare themselves with their peers. Significant industry-specific findings include:

- In the retail industry, only 35% of plans* have adopted an auto-enrollment feature, compared with 51% of plans across all industries.

- Within the finance and insurance industries, only 14% of participants have an outstanding loan, compared with 24% of participants across all industries.

- 77% of the manufacturing industry plans have adopted an auto-increase feature, compared with 69% of plans across all industries.

- Within the utilities industry, there is a 92% participation rate for plans with auto-enrollment, compared with 78% for non-auto-enrollment plans. This is a much smaller gap compared with all industries, which have an 88% participation rate with auto-enrollment and a 46% participation rate without.

REFERENCE POINT METHODOLOGY

Data are based on the large-market, full-service universe—TRP Total—of T. Rowe Price Retirement Plan Services, Inc., retirement plans (401(k) and 457 plans), consisting of 662 plans and over 1.6 million participants.

For plan-level analysis (e.g., averages by industry), a plan-weighted average is shown. This process takes the average from each plan and averages them together. A plan-weighted average assigns plans with a smaller number of participants the same weight as plans with a larger number of participants.

For participant-level analysis (e.g., averages by age and tenure), a participant-weighted average is shown. This process adds up all participants for all plans and takes one overall average. A participant weighted average assigns plans with a smaller number of participants less weight than plans with a larger number of participants.

Data and analysis cover the time periods spanning calendar years ended December 31, 2007, through December 31, 2015.

*Auto-increase and auto-enrollment data based on plans that are eligible to receive this service.

ABOUT T. ROWE PRICE RETIREMENT PLAN SERVICES, INC.

T. Rowe Price Retirement Plan Services, Inc. has been a retirement solutions provider for more than 30 years and currently serves nearly 1.9 million retirement plan participants across more than 3,500 plans. Retirement-related assets represent 69% of the firm’s total assets under management.

ABOUT T. ROWE PRICE

Founded in 1937, Baltimore-based T. Rowe Price Group, Inc. is a global investment management organization with $776.6 billion in assets under management as of June 30, 2016. The organization provides a broad array of mutual funds, subadvisory services, and separate account management for individual and institutional investors, retirement plans, and financial intermediaries. The company also offers sophisticated investment planning and guidance tools. T. Rowe Price’s disciplined, risk-aware investment approach focuses on diversification, style consistency, and fundamental research. For more information, visit troweprice.com, Twitter, YouTube,LinkedIn, or Facebook.