November 2023 / INVESTMENT INSIGHTS

Are US Stocks Worth the Price?

The Magnificent 7 have distorted US equity valuations

Key Insights

- At first glance, the S&P 500 Index’s elevated valuation could be concerning given the numerous headwinds facing equity markets.

- A deeper analysis reveals that a handful of mega-cap stocks in the S&P 500 Index have distorted US equity valuations, but their prices may not be unreasonable.

The resilient US economy has led to an improved earnings outlook for US stocks, but many investors worry that valuations—represented by the forward price-to-earnings (P/E) ratio—are too expensive given the uncertainty surrounding interest rates and the economy.

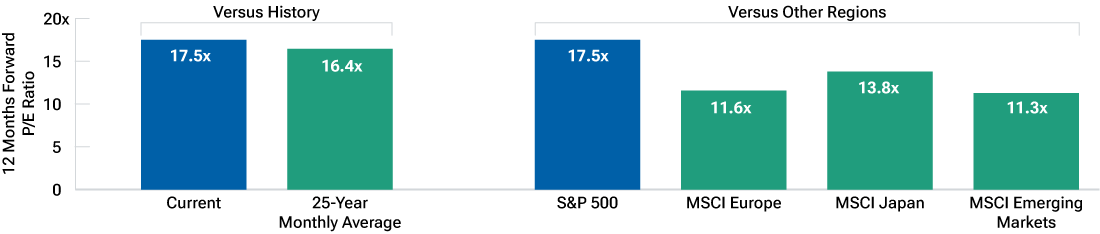

US stock valuations seem elevated relative to historical averages and to stocks in other regions of the world (Figure 1). But a deeper analysis of the S&P 500 Index reveals that a handful of mega-cap stocks that account for a large share of the index are responsible for the high valuations. This group of stocks—which includes Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla—has become widely known as the Magnificent 7.

US stocks look expensive

(Fig. 1) P/E ratio of US stocks relative to history and compared to other regions

As of October 23, 2023

Actual outcomes may differ materially from forward estimates.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. MSCI Indexes. See Additional Disclosures.

US stocks are represented by the S&P 500 Index.

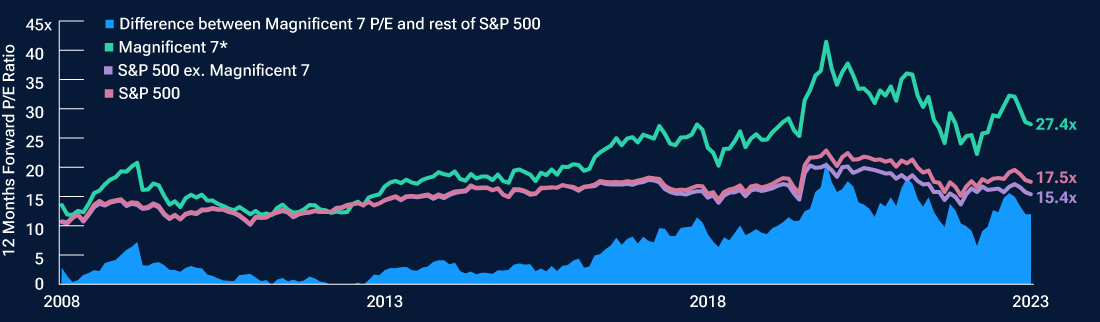

Collectively, the Magnificent 7 hold a P/E ratio that is considerably higher on a market cap-weighted basis than the S&P 500 Index. Without these seven stocks, the P/E ratio of the index is relatively modest (Figure 2). In other words, the broader US stock market does not look expensive through this lens; however, valuations for the Magnificent 7 look expensive.

Magnificent 7 have distorted US equity stock valuations

(Fig. 2) Comparing valuations of mega-cap stocks versus other S&P 500 stocks

January 1, 2008, through October 23, 2023.

Actual outcomes may differ materially from forward estimates.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. S&P 500 Index. See Additional Disclosures.

P/E ratios are market-cap weighted.

*The “Magnificent 7” stocks are Apple, Alphabet, Amazon.com, Meta Platforms, Microsoft, NVIDIA, and Tesla. The specific securities identified and described are for informational purposes only and do not represent recommendations. Not representative of an actual investment. There is no assurance that an investment in any security was or will be profitable.

Whether these elevated valuations are warranted is a difficult question to answer, but one simple way to provide a sanity check is to compare the P/E ratio of an index to its return on equity—a measure of how profitable and efficient a company has been over the past year. For the Magnificent 7, their high valuations were accompanied by similarly high market cap‑weighted returns on equity as of October 23. Whether these seven companies can sustain the level of profitability and efficiency that they have thus far exhibited remains to be seen.

When taken in context, the elevated valuations of US stocks in general and the Magnificent 7 collectively do not appear unreasonable. As a result, our Asset Allocation Committee currently holds a broadly neutral allocation to US equities despite elevated valuations amid an uncertain environment.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Tim Murray is a capital markets analyst in the Multi-Asset division at T. Rowe Price.