September 2023 / INVESTMENT INSIGHTS

Why the “High for Longer” Narrative Is Flawed

Central banks will likely ease sooner than expected

The market view on growth has undergone a furious transformation this year. In January, we were bracing ourselves for a hard landing. Then we were told to expect a soft landing. Now there is talk of “no landing”—i.e., that for growth to slow to a level that allows inflation to return to the 2% target, the core central banks must tighten further. I respectfully disagree: As I see it, the original hard landing narrative remains the correct one, and central banks will need to ease sooner rather than later.

There is no doubt that growth recovered impressively in the first half of the year. However, this does not mean—as some believe—that the global economy is now abundantly resilient and can cope comfortably with a sharp dose of central bank tightening. In my view, the growth rebound has been driven by three powerful forces that have temporarily loosened financial conditions but will soon fade. Let’s look at these more closely.

First, around the turn of the year, US and global inflation surprised on the downside. Second, the authorities in the world’s second‑largest economy, China, decided not only to abruptly reopen the economy, but also to roll back some of the measures designed to curb the all‑important residential construction sector. Third, the eurozone energy crisis confounded the experts by fading overnight. Combined, these three events produced a powerful bond and equity market rally. As sentiment changed, capital floated from the centre of the financial system to the periphery and financial conditions eased across the globe.

Unusual Recession, Unusual Recovery

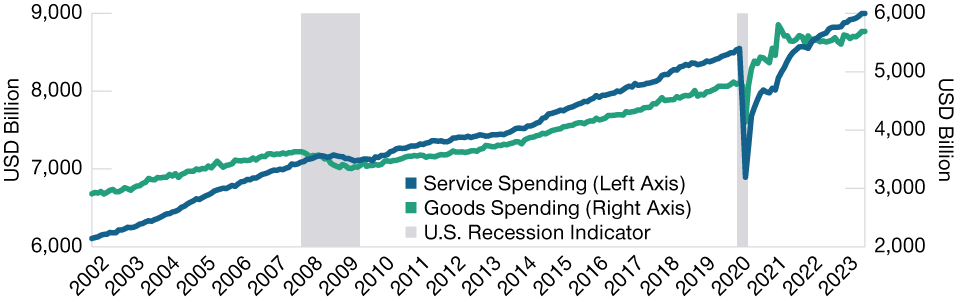

The economic response to this easing of conditions has been unusual in that the manufacturing sector has remained moribund while services have recovered sharply. This can be attributed to COVID. Traditional recessions damage the demand for goods, leading to a retracement of the manufacturing sector. As financial conditions eventually ease, the pent‑up demand for goods is released, resulting in a powerful cyclical recovery in manufacturing. By contrast, the COVID recession led to an unusual boom in manufacturing and a sharp retrenchment of the service sectors (Figure 1). Seen through this prism, the subsequent rebound in services is not a function of a structural change in the economy, but rather a natural response to the unusual nature of the COVID shock. The sharp recovery of the services sector explains the economy’s resilience to the abundant monetary tightening: Service sectors are labour-intensive, but the consumption of services is mostly unresponsive to changes in monetary policy.

Why the COVID Recession Was Different

(Fig. 1) Manufacturing boomed in the wake of the pandemic

As of August 31, 2023.

Source: U.S. Bureau of Economic Analysis.

I believe we are rapidly approaching the point at which service consumption returns to its natural level—indeed, there are already signs that the demand for services is slowing. What’s more, US households have almost exhausted their COVID transfers. My guess is that, as these dynamics run their course, we should be on the alert for a more pronounced slowdown. In other words, we may be about to discover that monetary policy has been calibrated to a world of extreme tailwinds and that these tailwinds are about to fade.

In addition, the forces that drove the easing of financial conditions around the turn of the year have started to fade. Courtesy of OPEC+ supply cuts, the oil price has now begun to increase, which will put upward pressure on headline inflation and erode households’ purchasing power. As the no‑landing narrative has unfolded, interest rates have sold off and the 30‑year US mortgage rate is back above the level of October 2022. Consequently, I expect a renewed weakening of both household demand and housing. Finally, the “China reopening” bounce has run its course, and as the residential construction sector continues to struggle under pressures to deleverage, the authorities are under renewed pressures to administer growth‑friendly policies. Although these policies are forthcoming, conservative management of fiscal and monetary policy has kept the pace of policy adjustment tepid.

Across the major economies, the narrative can be spilt into three parts. First, growth in China will remain somewhat muted as the overwriting policy priorities remain both to deleverage the economy and to shift economic dependence away from construction and toward the higher value‑added services sector. Second, Europe is moving quickly toward a recession, and I expect a meaningful weakening of European labour markets over the coming quarters. And third, the US economy remains the strongest, and amid moderation in growth, I expect the story of US exceptionalism to have further ground to cover.

Growth Will Slow as Monetary Conditions Tighten

If I am correct, we will soon be disabused of the notion that the economy can work just fine with the amount of monetary tightening that has been administered. As the penny drops, and growth surprises on the downside, we will see a substantial fall in the level of interest rates—most likely assisted by a shift toward easier monetary policy by the major central banks. This rally in rates will be associated with a steepening of core yield curves as investors reassess the need for monetary policy to be eased.

The most likely trajectory for equities is lower—as company earnings tend to follow economic growth, equities tend to prosper in environments with stronger growth. In the currency markets, for now, the US growth narrative remains the most resilient, and consequently, I expect the US dollar to remain the currency of choice. To return to the weaker US dollar world of earlier this year, the world requires a combination of either stronger growth in the eurozone and China or tangible steps toward interest rate cuts by the Federal Reserve without the expectation of an imminent US recession. In my view, the conditions for a weaker US dollar are quite far from being met today.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

September 2023 / MARKETS & ECONOMY

September 2023 / INVESTMENT INSIGHTS

Nikolaj Schmidt is the chief international economist in the Fixed Income Division of T. Rowe Price.