July 2023 / INVESTMENT INSIGHTS

US Equities Are Back in Favour

Earnings outlook for US companies is trending positive

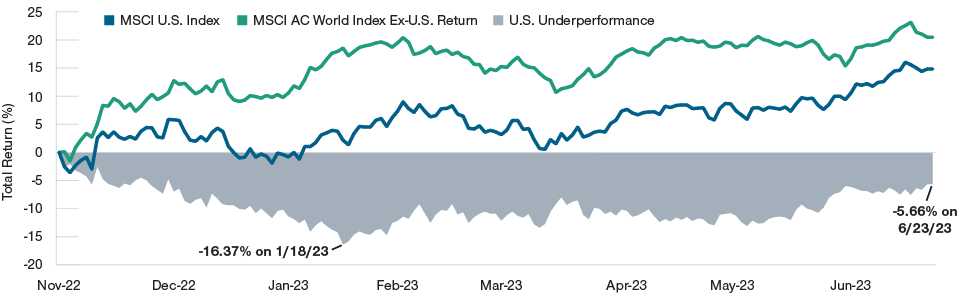

From late 2022 into 2023, non‑US equities—especially in Europe and China—significantly outpaced US stocks. However, the tailwinds that drove outperformance in those regions may be peaking. Meanwhile, US company earnings have rebounded after an extended period of deterioration. The gap in their performance relative to other global equities has narrowed by more than half (Figure 1).

U.S. Equities Bounce Back

(Fig. 1) U.S. equities vs. the rest of the world

November 1, 2022, through June 22, 2023.

Past performance is not a reliable indicator of future performance.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. MSCI Indexes. See Additional Disclosures.

European stocks rallied in early 2023, supported by sharply lower energy prices amid an unseasonably warm winter. But this price relief is likely to reverse as energy demand increases during the summer months. Colder temperatures in the coming 2023–2024 winter season also could boost energy consumption.

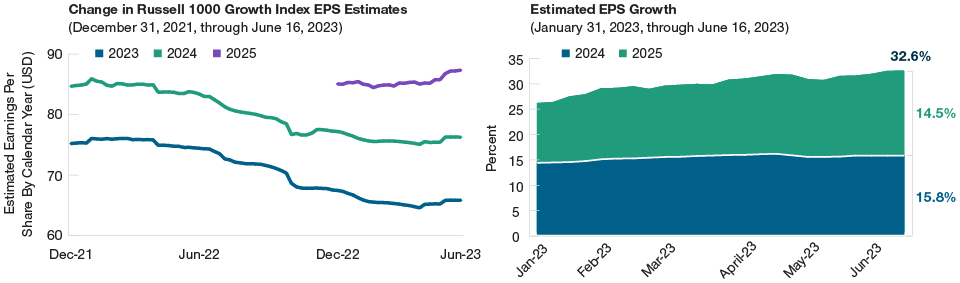

U.S. Growth Stocks Earnings Estimates Have Inflected Higher

(Fig. 2) Earnings outlook for U.S. growth stocks

Actual outcomes may differ materially from estimates. Estimates are subject to change.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. FTSE/Russell Indexes. See Additional Disclosures.

In China, robust economic activity driven by the post-COVID reopening appears to have faded, and stimulus measures to shore up economic weakness are unlikely to match prior levels given the government’s focus on financial deleveraging and ensuring that the benefits of economic growth are shared more widely.

Meanwhile, despite looming headwinds, the US economy has remained resilient, and the US earnings outlook is trending positive (Figure 2). US growth stocks, technology stocks in particular, have been boosted by recent developments in artificial intelligence. Companies in the US industrials sector also have benefited from higher demand spurred by the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, the Inflation Reduction Act, and corporate reshoring.

Notably, valuations for US stocks far exceed other global stocks. However, this valuation gap can be justified by differences in company profitability. US stocks are more expensive because they have enjoyed a sizable advantage in profitability—a gap that has been expanding gradually for nearly 15 years.

Given this improved outlook for US stocks, our Asset Allocation Committee moved its allocation to US stocks from underweight to neutral relative to the rest of the world.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

July 2023 / INVESTMENT INSIGHTS

Tim Murray is a capital markets analyst in the Multi-Asset division at T. Rowe Price.