March 2023 / INVESTMENT INSIGHTS

Building Core Strength to Meet Demands of Markets

Positioning across the style spectrum with a focus on individual stock picking

Key Insights

- Balancing both value and growth styles can help to mitigate portfolio risk and reduce the need for investors to have conviction in either style.

- We adopt a concentrated approach that demonstrates conviction and seeks to take advantage of the most actionable ideas from our global research platform.

- The strategy aims to deliver alpha by focusing on individual stocks versus large style or cyclical bets, offering potential to add value across different market environments.

Heightened market volatility challenged the conviction of asset allocators in 2022 as inflation ballooned to 40‑year highs and led the U.S. Federal Reserve to deliver some of the sharpest sets of interest rate hikes in recent history. The rising rate environment benefited value areas of the market, while punishing many growth stocks. However, even in a tough environment dominated by an exceptionally strong style effect, the Global Select Equity Composite kept pace with the MSCI World Index, eliminating the need for asset allocators to have conviction in either growth or value.

We operate a core approach that is style balanced between both growth and value stocks, which allows the opportunity to create alpha by focusing on individual stocks with idiosyncratic drivers of relative returns regardless of the market environment. This balanced approach helps to reduce the risk of being on the wrong side of any large style swings that can occur between growth and value.

A Concentrated Portfolio Demonstrates Conviction in Ideas

We believe focusing on investing in our best ideas can help deliver alpha in both up and down markets, as well as in markets that are led by growth or value. As a long‑term, bottom‑up investor, we want our stock selection to be the main driver of alpha and to not have the portfolio returns dictated by macro factors or style bets. Therefore, the strategy implements a high‑conviction, bottom‑up approach to portfolio management with a framework that emphasizes business quality and risk control. The representative portfolio is typically concentrated in 30–45 stocks and is designed to be less benchmark‑centric with high active share. Leveraging the best thinking of T. Rowe Price’s global research platform, we focus on stocks where we believe we have an edge and a potentially favorable risk‑adjusted return outcome.

While our focus is on idiosyncratic ideas, given our global mandate, we incorporate different types of stocks with different risk profiles and factor exposures into our analysis. Stock level risk and factor exposure is managed in concert with our detailed bottom‑up, fundamental analysis to ensure that the portfolio is not defined by style or macro‑specific outcomes. At a stock level, for example, some companies with large export‑oriented businesses have been hindered by the recent strength of the U.S. dollar, while there are companies that have suffered due to China’s zero‑COVID policy. More generally, higher inflation has negatively impacted companies as input costs have risen. Conversely, there have been clear beneficiaries of higher prices with energy companies a clear example. This reflects the bifurcation within equity markets and the types of risk we must balance to build a portfolio with alpha potential in varying market environments.

The Importance of Following Investment Principles and a Clear Investment Process

Our approach is to own proven, growing businesses that we believe can improve profitability and cash generation at attractive valuation points, but also to be sensitive when valuations may appear close to extreme levels, especially when managing our sell discipline.

When constructing a concentrated portfolio, it is crucial to understand the drivers behind stock performance. The macro variables that can drive stocks need to be balanced to control risk. We seek to create alpha by balancing unsystematic risk and focusing on companies that we believe are positioned to outperform relative to their peer group. Stock returns within the same sector or industry can exhibit notable dispersion, so we aim to identify the durable and resilient companies that can demonstrate pricing power, barriers to entry, and sustainable advantages over time. Research is crucial here to figure out who has, or is developing, an advantage and is winning in their marketplaces. This helps to refine stock‑picking ideas considerably.

This research is also immensely useful when stocks are undergoing periods of distressed sentiment but transitioning to a better outlook. While it is always tempting to wait for patterns of recovery to be established, early identification of fundamentals stabilizing, or the “stop getting worse” point, is crucial to return generation.

In all cases, we would emphasize our desire to remain disciplined around valuation and remain continuously engaged with companies. Not only is it important to meet companies face to face, visit their stores and factories, etc., but we also need to meet with their competitors at the same time to build a complete picture of the opportunity set.

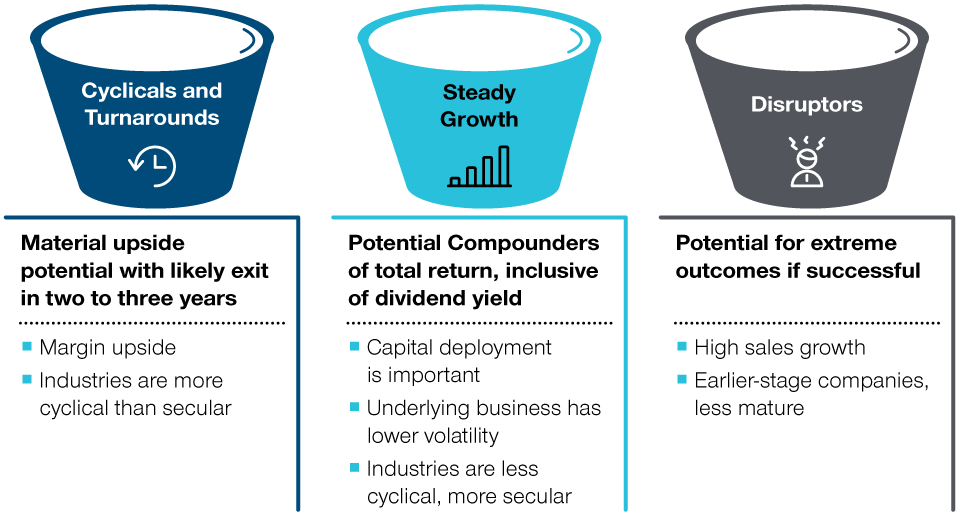

Diversified Exposure to Achieve Balance in the Portfolio

We define our core approach through three distinct buckets—cyclicals and turnarounds, steady growth, and disruptors—with the market dictating where opportunities present themselves. Cyclical and turnaround exposure is focused on companies where, through our research, we have identified positive cyclical or structural change factors that mean a stock is worthy of a rerating. Most common within the steady growth bucket are companies that have established business models, can demonstrate a clear strategy, and can exhibit good execution and earnings growth through a business cycle. Finally, within disruptors, we are looking for businesses that are gaining share, that have a large addressable market, and where there are opportunities for extreme outcomes.

Diversified Exposure to Achieve Balance

Three distinct buckets focusing on the best market opportunities

As of March 2023.

For illustrative purposes only.

Source: T. Rowe Price.

Our holdings are generally focused on well‑established businesses that are profitable, which means we have an inherent bias toward mid‑ and large‑cap companies. We also have a focus on “quality companies” with good balance sheets as empirical evidence has shown that high‑quality companies often outperform lower‑quality ones over the long term. There are differences in market environments, with quality rewarded in down or flat markets and less so in up markets, but a pattern of historical outperformance can be clearly identified over the long term.

Ability to Deliver in Variable Market Environments

Over the last two years, equity investors have experienced a performance roller coaster defined by sharp shifts driven by rapidly changing macro and factor dynamics. It has served as a painful reminder of the risks tied to strategies blindly following a factor or theme. We have seen periods where growth meaningfully outperformed and periods where value has outperformed. Through it all, we have been able to effectively navigate multiple market leadership changes by largely avoiding portfolio‑defining macro variable exposure to deliver on our goal of adding value through stock selection. We believe, with that focus on stock picking across the style spectrum, that we can continue to balance those macro and style factors as we seek to add value across different market environments.

The representative portfolio is an account in the composite we believe most closely reflects current portfolio management style for the strategy. Performance is not a consideration in the selection of the representative portfolio. The characteristics of the representative portfolio shown may differ from those of other accounts in the strategy. Please see the GIPS® Composite Report for additional information on the composite.

Risks—The following risks are materially relevant to the portfolio:

Currency—Currency exchange rate movements could reduce investment gains or increase investment losses.

Emerging markets—Emerging markets are less established than developed markets and therefore involve higher risks.

Issuer concentration—Issuer concentration risk may result in performance being more strongly affected by any business, industry, economic, financial or market conditions affecting those issuers in which the portfolio’s assets are concentrated.

Sector concentration—Sector concentration risk may result in performance being more strongly affected by any business, industry, economic, financial or market conditions affecting a particular sector in which the portfolio’s assets are concentrated.

Small and mid‑cap—Small and mid‑size company stock prices can be more volatile than stock prices of larger companies.

General Portfolio Risks:

Equity—Equities can lose value rapidly for a variety of reasons and can remain at low prices indefinitely.

ESG and sustainability—ESG and Sustainability risk may result in a material negative impact on the value of an investment and performance of the portfolio.

Geographic concentration—Geographic concentration risk may result in performance being more strongly affected by any social, political, economic, environmental or market conditions affecting those countries or regions in which the portfolio’s assets are concentrated.

Hedging—Hedging measures involve costs and may work imperfectly, may not be feasible at times, or may fail completely.

Investment portfolio—Investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management—Management risk may result in potential conflicts of interest relating to the obligations of the investment manager.

Market—Market risk may subject the portfolio to experience losses caused by unexpected changes in a wide variety of factors.

Operational—Operational risk may cause losses as a result of incidents caused by people, systems, and/or processes.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

March 2023 / INVESTMENT INSIGHTS

Peter Bates is the portfolio manager of the Global Select Equity Strategy in the International Equity Division . He is a vice president and Investment Advisory Committee member of the US Dividend Growth Equity, US Large-Cap Core Equity, and US Value Equity Strategies. In addition, he is a member of the Investment Advisory Committees of the Global Growth Equity, Global Focused Growth Equity, and Japan Equity Strategies. Peter is a vice president of T. Rowe Price Group, Inc., and an executive vice president of T. Rowe Price International Ltd.