September 2022 / INVESTMENT INSIGHTS

Contrarian Investing During a Sell-Off: An Update

High inflation and rising rates complicate the analysis

Key Insights

- Market declines in the first half of 2022 may have left some investors wondering if the time is right to raise exposure to stocks and other risk assets.

- Our earlier study of historical sell‑offs found that adding equity exposure typically enhanced returns, even if the exact timing was early or late.

- Narrowing our focus to five past sell‑offs that also featured high inflation and rising interest rates suggests a more cautious approach may be needed now.

The first half of 2022 was a particularly challenging period for investors. High inflation, coupled with extended equity valuations and rising U.S. interest rates, led to twin sell‑offs across both stocks and bonds. In the wake of such a significant market drawdown, many investors might be wondering if the time is right to lean back into stocks and other risk assets.

While T. Rowe Price takes a long‑term strategic approach to portfolio design, we do believe that tactical asset allocation can enhance returns by taking advantage of shorter‑term relative value opportunities—such as those that potentially may be created in severe market drawdowns.

However, few, if any, investors can successfully identify the precise trough of an extended market drawdown. This raises the question: What are the potential penalties for being too early or too late in making a tactical shift?

We previously examined this issue after the COVID‑19 pandemic generated a major sell‑off in U.S. and global equities in the first quarter of 2020.1 In that study, we looked at returns following 17 prior U.S. market declines in which the S&P 500 Index sold off by 15% or more, beginning with the 1929 crash and ending with the December 2018 market correction. More recently, we updated our analysis to include the COVID‑19 sell-off (Figure 1).2

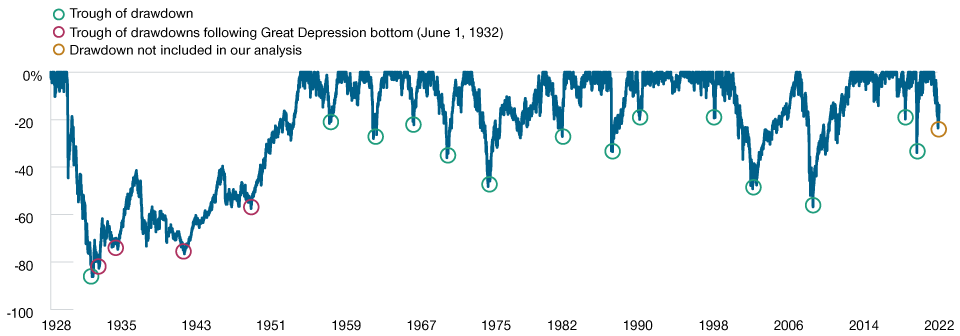

The Bear Facts: Major U.S. Equity Sell‑Offs Since 1928

(Fig. 1) Historical drawdowns of 15% or more in the S&P 500 Index*

Past performance is not a reliable indicator of future performance.

As of July 31, 2022.

*We used S&P 500 Index price data from January 3, 1928, through July 31, 2022, to identify drawdowns of 15% or more from a previous absolute market peak. We then identified the date marking the trough for each drawdown. However, in order to capture market sell‑offs during and immediately after the Great Depression (with troughs on February 27, 1933, March 14, 1935, April 28, 1942, and June 13, 1949), we set June 1, 1932, as the new floor and identified subsequent market peaks and drawdowns from that date. The most recent S&P 500 sell‑off—the market drawdown in early 2022—was not included in our analysis. The most recent trough is marked as not included in the analysis (yellow circle in key)

Source: Bloomberg Finance L.P. (see Additional Disclosures). All data analysis by T. Rowe Price.

Surprisingly, we found that investors could have added U.S. equity exposure in their portfolios anywhere from three months before to three months after the absolute trough in all 18 market drawdowns (including the COVID‑19 sell-off) and still enhanced returns, on average, over the following 12 months.

However, economic fundamentals matter—and high inflation and rising interest rates present a particularly challenging environment for risk assets. That being the case, we narrowed the focus of our analysis to five historical U.S. equity market drawdowns that occurred during periods of high inflation and high and/or rising interest rates. In our view, the results of this targeted study suggest that a little more patience may be required before increasing exposure to equities and other risk assets in the current market environment.

Reflecting this view, the T. Rowe Price Asset Allocation Committee (AAC) continued to hold an underweight position in stocks relative to bonds as of July 31, 2022. However, going forward, the AAC may consider raising equity exposure in its positioning if it observes some combination of a less aggressively hawkish U.S. Federal Reserve and an improvement in economic and earnings visibility.

Lessons From History

In both our original and our updated tactical analysis, we recognized that for most investors, tactical investment decisions are likely to be made in the context of their long‑term strategic allocations—not as a shift from 100% to 0% exposure in favor of stocks or bonds. Accordingly, both of our studies assume that an investor tactically shifted from a hypothetical 60% U.S. stocks/40% U.S. bonds (60/40) allocation to a hypothetical 70% U.S. stocks/30% U.S. bonds (70/30) mix whenever they believed the market had reached a drawdown trough.3

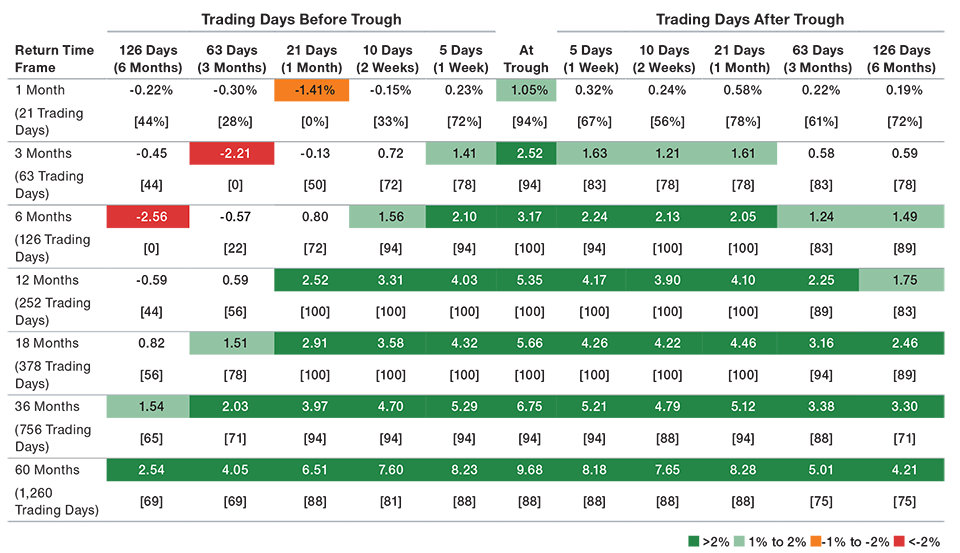

Adding U.S. Equity Exposure in Past Sell‑Offs Typically Boosted Returns

(Fig. 2) Average cumulative return differentials and [success rates] for a hypothetical 70% U.S. stock/30% U.S. bond allocation versus a hypothetical 60%/40% portfolio*

Past performance is not a reliable indicator of future performance.

As of July 31, 2022.

*The 2020 COVID‑19 sell-off was the most recent event examined in our analysis. However, 36‑month and 60‑month returns were not yet available for the starting points shown before and after the trough of that downturn. Similarly, 60‑month returns were not yet available for starting points before and after the trough of the December 2018 market sell-off. Accordingly, results for those periods are not included in the averages above.

Sources: Bloomberg Finance L.P., Morningstar (see Additional Disclosures), and U.S. Treasury/Haver Analytics.

The chart above is shown for illustrative purposes only, does not represent an actual investment, and does not reflect fees and costs of a portfolio.

Actual investment results may vary. See important disclosures at the end. Equity returns based on daily S&P 500 Index total returns from January 3, 1928,

through July 31, 2022. Fixed income returns based on an estimate of daily interpolated returns for the Ibbotson Intermediate Government Bond Index from

January 3, 1928, through December 29, 1961, and on daily total returns for the 5‑year U.S. Treasury note where daily data were available from January 2, 1962,

through July 31, 2022. The return differentials shown above are measured between the cumulative total returns for a hypothetical 70% U.S. stock/30% U.S. bond portfolio and a hypothetical 60%/40% portfolio in the periods shown, averaged across 18 major historical U.S. equity sell-offs. A major sell‑off was defined as a decline of 15% or more in the S&P 500 Index. The success rate is the percentage of performance periods in which the 70/30 hypothetical portfolio outperformed the 60/40 hypothetical portfolio. Results shown were derived from daily rebalancing and daily cumulative returns.

We then measured potential cumulative returns on the hypothetical 70/30 portfolio relative to the hypothetical 60/40 portfolio over various time periods beginning before and after each market trough to show the impact of being early or late in a timing decision. These returns were averaged across all 18 of the drawdowns we examined (Figure 2). Updating the broader analysis to include the COVID‑19 sell‑off did not significantly alter the results.

Our broad study found that if a hypothetical investor timed market troughs perfectly—i.e., shifted from the hypothetical 60/40 portfolio to the hypothetical 70/30 allocation mix on the exact date of each of the 18 troughs we examined—the tactical gains could have been quite high across most time frames. For example:

- Over the 12 months following the trough, the investor who shifted to a hypothetical 70/30 allocation could have earned an average 535 basis points (bps) of excess return, gross of fees, relative to the 60/40 portfolio.

- The 70/30 mix would have outperformed the 60/40 portfolio over the 12 months following the trough in all 18 of the sell‑offs we examined—a 100% success rate.

An even more important finding in our broader analysis was that historically it wasn’t necessary to time drawdowns precisely in order to generate significant excess returns :

- If our hypothetical investor had shifted to a 70/30 allocation one month (21 trading days) before the exact market trough, subsequent 12‑month excess returns across the 18 drawdowns could have been 252 bps higher, on average, than if they had stuck with a 60/40 allocation.

- Raising equity exposure one month after the trough produced roughly similar results, although 12‑month excess returns for the 70/30 allocation could have been even higher—an average 410 bps relative to the 60/40 portfolio.

- In both cases—one month before and one month after the trough—the 70/30 allocation outperformed the 60/40 portfolio in 100% of the 12‑month periods we examined.

Applying Our Framework to the Current Sell‑Off

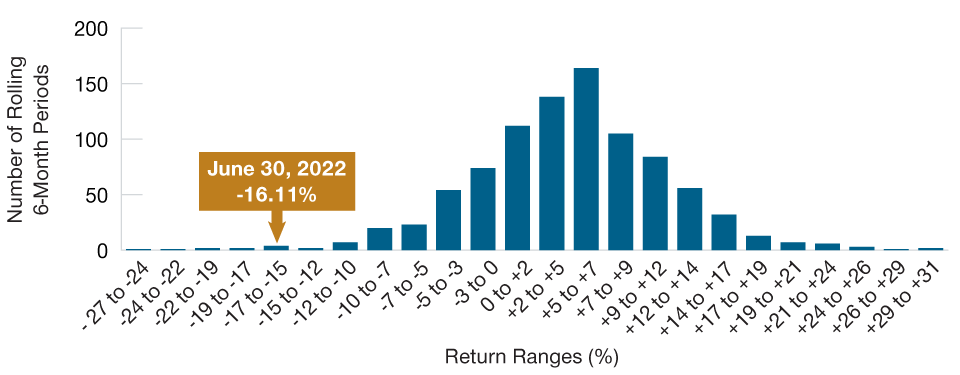

The financial market declines seen in early 2022 were particularly steep in a historical context. Over the six months ended June 30, 2022, a hypothetical 60/40 portfolio (represented by the S&P 500 Index and the Bloomberg U.S. Aggregate Bond Index) returned -16.11%,4 a result that fell within the lowest percentile of returns for all historical rolling six‑month periods since 1945. (Figure 3).

Recent U.S. Equity and Fixed Income Losses Were Near the Extreme of Their Historical Range

(Fig. 3) Distribution of rolling six‑month returns for a hypothetical 60% U.S.

stock/40% U.S. bond portfolio

Past performance is not a reliable indicator of future performance. The chart above is shown for illustrative purposes only, does not represent an actual investment, and does not reflect fees and costs of a portfolio. Actual investment results may vary. See important disclosures at the end.

December 31, 1945, through June 30, 2022

Sources: Standard & Poor’s, Morningstar, and Bloomberg Finance L.P. (see Additional Disclosures).Equity returns are represented by the S&P 500 Index. Bond returns are represented by the Ibbotson Intermediate Government Bond Index (January 1946 through December 1975) and the Bloomberg U.S.

If returns on the 60/40 portfolio were distributed normally (that is, across a smooth bell‑shaped curve), a six‑month loss of such magnitude would be expected to occur only once every 304 years. However, the existence of “fat tails” (disproportionally large numbers of extreme values) challenges the assumption of a normal distribution for financial asset returns.

The unusually sharp equity declines of early 2022 were accompanied by—and driven by—exceptionally high inflation, as global energy and food prices jumped in the wake of Russia’s invasion of Ukraine. The U.S. consumer price index (CPI) rose 9% over the 12 months ending in June 2022—the fastest increase in more than four decades.

Reacting to these inflation dynamics, the U.S. Federal Reserve moved quickly to tighten monetary policy, producing a dramatic spike in U.S. Treasury yields. The yield on the 10‑year U.S. Treasury note nearly doubled in the first six months of 2022 before easing at the start of the second quarter.

In light of these conditions, we decided to narrow our analysis to look at previous U.S. market drawdowns that posed similar challenges for equity investors. This focus led us to concentrate on five historical U.S. equity sell‑offs that featured both high inflation and rising interest rates—conditions similar to those that have defined the 2022 market environment, in our view (Figure 4).5

The Early 2022 Sell‑Off Resembled Past High Inflation Downturns

(Fig. 4) U.S. consumer price index (CPI) and 10‑year Treasury yield at market troughs

Past performance is not a reliable indicator of future performance.

As of July 31, 2022.

*Not included in study. Trough date may change.

Sources: Federal Reserve Bank of St. Louis, T. Rowe Price calculations using data from FactSet Research

Systems Inc. All rights reserved.

The results of our new analysis can be found in Figure 5. They suggest that a more patient approach to buying stocks may be warranted when the underlying inflation and interest rate fundamentals are unusually poor.

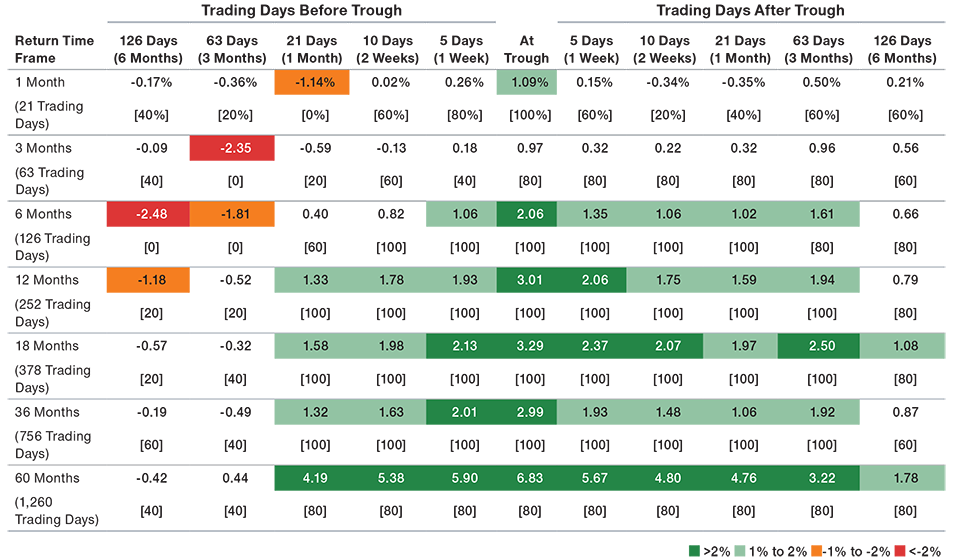

Caution May Be Needed When Inflation Is High and Interest Rates Are Rising

(Fig. 5) Average cumulative return differentials and [success rates] across five high‑inflation, rising‑rate U.S. equity sell‑offs

Past performance is not a reliable indicator of future performance.

As of July 31, 2022.

Sources: Bloomberg Finance L.P., Morningstar (see Additional Disclosures), and U.S. Treasury/Haver Analytics.

The chart above is shown for illustrative purposes only, does not represent an actual investment, and does not reflect fees and costs of a portfolio.

Actual investment results may vary. See important disclosures at the end. Equity and fixed income returns, return differentials, and success rates are based

on the same benchmarks used in Figure 2. The results shown here are averaged across the five major historical U.S. equity sell-offs shown in Figure 4, which

featured declines of 15% or more in the S&P 500 Index during periods of high inflation and rising interest rates as measured by the yield on the 10‑year Treasury note. High inflation was defined as a year‑over‑year reading of more than 4% in the U.S. CPI at the time of the market trough

For example, when we examined the performance of an investor who shifted from a hypothetical 60/40 portfolio to a 70/30 allocation three months (63 trading days) before the trough of a high inflation/rising interest rate drawdown, we found that:

- They could have reduced excess returns by an average 52 bps over the following 12‑month period, versus a 59 bps average return gain across the full sample of 18 drawdowns.

- The hypothetical 70/30 allocation would have outperformed the 60/40 portfolio in only 20% of all following 12‑month periods, versus a 56% success rate across the full sample.

- Negative excess returns could have been experienced for at least three years following the shift to a 70/30 hypothetical portfolio allocation.

Compared with the full sample, we also found a less compelling case for being early, as opposed to late, in high inflation/rising rate sell‑offs. Indeed, there appeared to be asymmetric benefits to adding to equities after the market trough.

For example, an investor who shifted to a hypothetical 70/30 allocation three months after the trough of a high inflation/rising rate drawdown could have enhanced 12‑month forward excess returns by an average 194 basis points, versus a 52 bps reduction from making the same shift three months before the trough.

While the sample size of high inflation/rising rate sell‑offs is admittedly small, the results of our updated analysis still suggest to us that investors could benefit from being more patient during such drawdowns.

Our Tactical Positioning

Around the trough of the COVID‑19 sell‑off in March 2020, the AAC gradually raised global equity exposure in its asset allocation positioning as market values moved lower. Some of these contrarian moves were early, others closer to the trough, but each of them reflected the committee’s perception that value could be added in a dislocated market, even if the timing was not exactly correct.

In the most recent U.S. equity sell-off, the S&P 500 Index reached a 23.6% peak‑to‑trough decline on June 16, 2022. The market then rallied, with the S&P 500 rising almost 8% through August 31, 2022. Through these moves, the AAC remained tactically underweight both U.S. and global equities. Key factors behind this relatively cautious approach included:

- Our perception that the Fed couldn’t rescue the financial markets by cutting interest rates because it will need to continue fighting inflation.

- Although equities repriced to reflect higher interest rates, broad price/earnings ratios and other multiples only fell to near their historical averages—limiting perceived relative valuation opportunities.

- Corporate earnings estimates appeared optimistic in the committee’s view, considering the risks of U.S. and/or global recessions and the potential downward pressure on profit margins.

In the AAC’s view, these factors created enough uncertainty about how far we are from a true market bottom to justify a cautious approach, both before and after the June trough. However, the committee stands ready to increase equity exposure if it believes these conditions have changed.

We also would note that while stock and bond positioning often takes the headline, the AAC’s approach to tactical allocation is considerably more nuanced than that. For example, the committee recently added duration by neutralizing a previous underweight to long‑term U.S. Treasuries. As of July 31, 2022, the committee’s positioning also featured tactical overweights in high yield and other “spread” fixed income sectors, where it believes that current yields and credit spreads provide adequate potential compensation for the perceived risks. The latter position highlights the importance of fundamental credit research in potentially helping to moderate the headwinds of a corporate credit cycle.

Conclusions

Projecting forward market returns is a challenging task that requires investors to balance historical data and their assumptions about future market dynamics. Our original study found that raising equity allocations in significant market sell‑offs typically enhanced returns irrespective of the precise timing. However, when we narrowed the analysis to the historical market drawdowns that most resembled the most recent one—featuring a combination of high inflation and rising and/or high interest rates—our conclusions became more nuanced and suggested a more patient approach.

We should note that T. Rowe Price does not have a single “house view” on these issues. While the AAC remains underweight stocks in its positioning, some individual portfolio managers may be increasing equity exposure in their own strategies.

While the current environment warrants caution, in our view, we continue to believe that investors who increase their exposure to risk assets during market sell‑offs potentially can enhance long‑term portfolio returns. Accordingly, we will continue to monitor economic and market factors to identify potential opportunities to increase equity exposure as the cycle evolves.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

September 2022 / ASSET ALLOCATION VIEWPOINT

Sebastien Page is head of Global Multi-Asset and Chair of the Asset Allocation Steering Committee, which is responsible for management and oversight of the Multi-Asset Division. Before joining our firm Mr. Page was Executive Vice President at PIMCO.

Som Priestley is a portfolio manager and multi-asset solutions strategist in the Multi-Asset Division of T. Rowe Price.