February 2022 / INVESTMENT INSIGHTS

Why Impact Investing Needs Public Debt Markets

Their size and diversified nature can foster long-term change

Key Insights

- Impact investing is often closely linked to private markets. However, this ignores the potential that public debt capital can afford investors and issuers.

- The vast size and depth of public markets, on top of greater liquidity, can help asset managers find opportunities that can make a material impact on the United Nations Sustainable Development Goals.

- For issuers, public markets can provide a deeper pool of capital to help fund their day‑to‑day businesses while helping them meet their long‑term impact goals.

Fixed income has traditionally presented a distinct well of opportunity within impact investing, an advancement on environmental, social, and governance (ESG) finance that combines investing with the intention of generating positive and measurable impact in an environmental or social context along with a positive return. Historically, debt has outstripped equity and real estate by significant margins in terms of investments made and amounts spent in the realm of impact investing. However, attention has typically focused on the private side of debt capital markets.

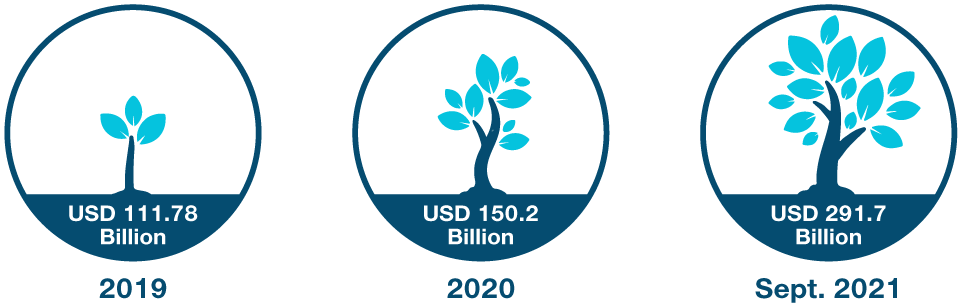

Impact Investors Are Branching Out Into Public Debt Markets

(Fig. 1) Global corporate ESG issuance in 2021 has already almost doubled last year’s figure

As of September 30, 2021. Includes corporate issuance greater than USD 300 million only. Source: Bloomberg Finance L.P. Analysis by T. Rowe Price.

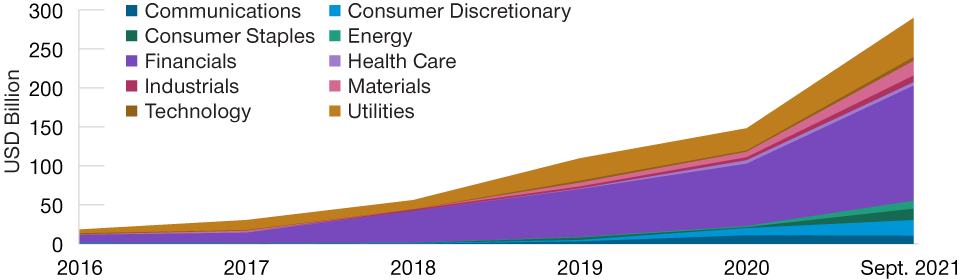

Impact Opportunities in Public Markets Are Becoming Deeper and More Diverse

(Fig. 2) ESG issuance among global corporates now covers more sectors than before

As of September 30, 2021. Includes corporate issuance greater than USD 300 million only. Source: Bloomberg Finance L.P. Analysis by T. Rowe Price.

In our view, this unduly takes the spotlight from the potential of publicly traded debt markets, which we believe offer investors a vast and deep range of potential companies. Issuers and investors can find more opportunities, issue more debt, potentially benefit from greater liquidity, and potentially deliver larger material impacts than if they rely solely on the private markets.

Deep Markets Can Help Tackle Problems on a Global Scale

The extent to which public markets can augment the range of impact opportunities can be seen by the growing scale of ESG‑focused goals. Over the last few years, the rise of ESG‑focused investment strategies has seen many asset managers look to align their activities with the UN SDGs, a recognized framework designed to achieve targets around global challenges such as climate change, poverty, and financial inclusion. Indeed, according to a 2019 BNP Paribas survey, 65% of managers with ESG strategies align their investment framework with the SDGs, often with SDG‑linked revenue targets for portfolio companies. Altogether, the UN estimates that the amount of investment required to achieve these SDGs by 2030 would be USD 5 trillion to USD 7 trillion per year.

Achieving these lofty goals will be a significant challenge in the decades ahead; however, from an investing perspective, public debt markets could offer the depth of capital needed to grow impact investing at the necessary scale. Across both corporates and sovereigns, global ESG bond issuance after the first nine months of 2021 is on pace to more than double 2020’s total issuance, as well as almost break the USD 1 trillion barrier. By contrast, private market data provider Preqin suggests that entire assets under management for private debt investors totaled a shade under USD 900 billion at the end of 2020. For impact investors, the acceleration of publicly traded ESG‑labeled debt suggests that is where the bulk of opportunities could come in the future, particularly with the SDGs in mind.

Public Markets Present a Wider Variety of Opportunities

This greater market depth in terms of issuance amount is complemented by the wider breadth of opportunities in terms of industries. Indeed, although ESG corporate issuance declined somewhat quarter on quarter in Q3, year-on-year growth is at around 115%, compared with around 45% for sovereign‑issued labeled bonds according to T. Rowe Price analysis. Looking at corporate sectors in isolation, the number of industries seeing ESG issuance has doubled over the last six years, with issuance rising from USD 5.3 billion in 2015 to over USD 291.7 billion in the first nine months of 2021 alone during that timeframe.

Notable publicly traded ESG‑related deals include German automotive giant Daimler’s EUR 1.2 billion green issue in March to finance climate and electric vehicle targets. More recently, Italian energy firm Eni issued the first sustainability‑linked bond in its sector, worth around EUR 1 billion and linked to carbon footprint and renewable energy targets. As overall value and volume of ESG issuance in public debt markets continues to grow, we believe so will the potential scope and breadth of the opportunities by sector, size, and geography.

Making an Impact Post‑investment

Higher liquidity is another key advantage of public debt markets when it comes to impact investing. Ongoing daily pricing and the sheer volume of deals for public credits every day, for example, creates a market where issuers and investors are cognizant of what reflects fair value, something private markets typically do not afford. In addition, public markets can provide investors with not just a more liquid environment to exit an investment, but also pass on the obligation to another investor with aligned values.

Achieving the UN’s SDGs will require enormous investment and capital expenditure across the investor, corporate, and sovereign communities. While private markets will have a role to play, we believe that the size of the task at hand means that public credit markets should become the focus of attention for impact investors. The breadth, depth, and liquidity they provide give investors the opportunity to access a wider variety of ESG‑linked opportunities, while also potentially providing issuers with enough capital to concurrently run their businesses and invest in long‑term impact goals.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Matt Lawton is a portfolio manager in the Fixed Income Division. He manages the Global Impact Credit Strategy and co-manages the US Investment Grade Corporate Bond Strategy. Matt is a vice president and member of the Investment Advisory Committees for the Corporate Income, New Income, and Ultra Short-Term Bond Funds, and he is a vice president of the Short-Term Bond Fund. He also is a member of the Fixed Income ESG Steering and Advisory and the ESG Committees. Matt is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Associates, Inc.