April 2021 / MARKETS & ECONOMY

Leveraging a Diversity of Perspectives on Rising Rates

An unusual rebound may provide opportunities even as rates rise

Key Insights

- T. Rowe Price investment professionals have varying views on the recent increase in Treasury yields but expect an atypical economic rebound later in 2021.

- We highlight viewpoints related to inflation protected securities, the Treasury yield curve, dividend-paying stocks, emerging markets, and the Federal Reserve.

- We believe that our diversity of views on the implications of rising rates can give our investment professionals an advantage in this unusual environment.

Just as the sudden shutdown of much of the global economy at the onset of the coronavirus pandemic in 2020 was unprecedented, the expected recovery in 2021 is likely to be unique. Developed market central banks seem determined to maintain their extremely accommodative monetary policies, and fiscal stimulus in many countries—as evidenced most recently by the USD 1.9 trillion spending package in the U.S.—should make the economic rebound much more robust than previous recoveries. With the consumer saving rate at record highs in the U.S., pent-up demand could also help drive growth as accelerating vaccinations support economic reopening.

But what does this mean for financial markets? U.S. Treasury yields have increased markedly in early 2021, with the yield on the benchmark 10-year Treasury note climbing from 0.93% at the end of December 2020 to around 1.70% in mid-March 2021. By placing a greater discount on future earnings, higher yields have helped accelerate the rotation away from higher-valuation tech stocks and toward value stocks.

Some T. Rowe Price investment professionals see the rising rates as an indicator of meaningfully higher longer-term inflation expectations, while others view the move as simply a healthy reflection of the expected increase in growth as global economies recover. This range of perspectives can help portfolio managers evaluate the potential for scenarios that may not exactly align with their own outlook. Here’s what our investment professionals are saying.

Potential for Inflation to Exceed Anticipated Increase

Economists widely expect inflation data to show relatively large price increases beginning in the second quarter in comparison with the year-earlier period, when consumer prices broadly fell. However, most see inflation settling at lower levels in the longer term.

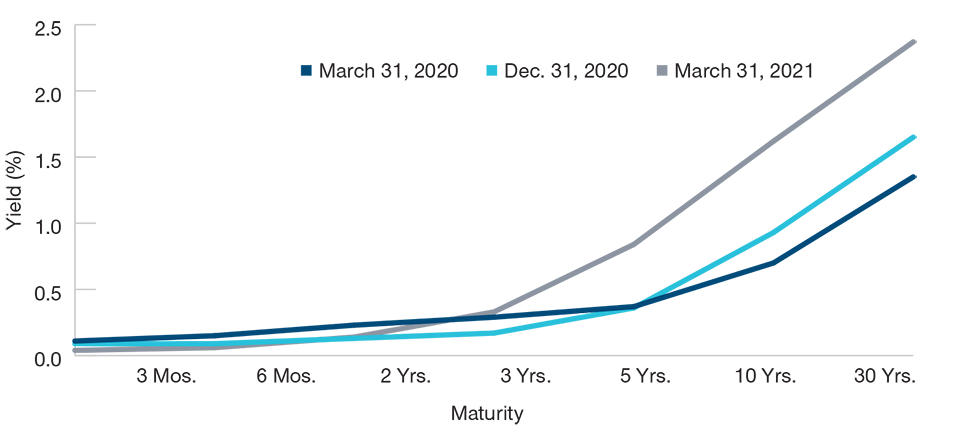

Increasing Longer-Term Treasury Yields

(Fig. 1) U.S. Treasury yield curves have steepened

Past performance is not a reliable indicator of future performance.

As of March 15, 2021.

Source: Federal Reserve Board.

Michael Sewell, portfolio manager of the US Inflation Protected Bond and US Short-Term Inflation Focused Bond Strategies, sees the potential for inflation to exceed even the broadly anticipated increase in 2021. This could cause consumers to adjust their expectations for inflation going forward, leading to structurally higher longer-term inflation levels.

Mike says that Treasury inflation protected securities (TIPS) would likely perform well in an environment where actual inflation exceeds market expectations. In terms of investors’ broad asset allocations, he believes that TIPS are an effective hedge against interest rate risk because they should be poised to outperform nominal (not inflation-adjusted) Treasuries in an environment where stronger growth and inflation concerns pressure nominal rates higher. In addition, in his view, inflation protected bonds can potentially also act as a hedge against downturns in risk assets if inflation exceeds expectations and begins to pressure corporate profits.

Portfolio Allocations That Benefit From Inflation

Similarly, Tim Murray, capital markets strategist in our Multi-Asset Division, sees consumers exiting the pandemic with a remarkable savings glut, likely leading to a sudden increase in spending that could lead to rising prices. He anticipates that longer-term inflation will tend to rise above the abnormally low levels seen over the past decade.

Tim believes that investors may want to consider increasing their portfolio allocations to asset classes that could benefit from higher inflation, including TIPS and value, small-cap, and emerging market equities. He also believes that “real assets”—which include natural resources and real estate equities—have the potential to maintain or gain value during periods of high inflation, making them useful hedges in an inflationary environment.

Yield Curve Could Steepen Further

Although longer-term Treasury yields have increased this year, shorter-maturity yields have stayed relatively steady. As a result, the Treasury yield curve, which measures the difference between short- and long-term yields, has steepened.

Alex Obaza, portfolio manager of the US Ultra-Short Term Bond Strategy, observes that the dynamics of yield curve steepening have changed since the global financial crisis (GFC). Prior to the GFC, the yield curve typically steepened when the Federal Reserve cut interest rates and short-term yields decreased in line with the federal funds rate. But the Fed slashed rates to near zero during the GFC, where they have generally stayed. The near-zero federal funds rate now holds short-term Treasury yields nearly steady as longer-maturity yields fluctuate in response to market expectations for economic growth and inflation.

Alex also analyzed post-GFC periods when the yield curve steepened and compared the size of those moves with the current trend. Although segments of the yield curve have steepened more than post-GFC averages (as of mid-March), Alex and US Core Bond Strategy Portfolio Manager Steve Bartolini see room for the steepening to continue. They note that the economic backdrop is stronger than it was following the GFC and during other post-GFC periods of yield curve steepening, with a variety of metrics measuring employment, manufacturing, and inflation expectations increasing at a greater pace.

Focus on Stocks Increasing Their Dividends

US Dividend Growth Equity Strategy Portfolio Manager Tom Huber acknowledges that inflationary pressure and higher interest rates could lure some income-seeking investors away from stocks where an above-average dividend yield has typically accounted for the bulk of total returns. However, he concentrates on finding companies that he believes are increasing their dividends, not just those with high dividends.

Tom says that, in fact, higher rates could boost some sectors, such as financials. Banks stand to benefit from an expected increase in lending activity as the economy recovers as well as from healthier net interest margins stemming from higher longer-term rates and a steeper yield curve. While these factors could temporarily boost most bank stocks, Tom tends to focus on company-specific drivers and characteristics that he believes can help position a financial institution for an extended period of sustained growth.

Higher Inflation Could Pressure Some EM Central Banks to Raise Rates

Inflation could also affect emerging markets (EMs). Andrew Keirle, Emerging Markets Local Currency Bond Strategy portfolio manager, expects the recovery in oil prices to push headline inflation rates moderately higher in EMs over the next few months. However, in his view, core inflation—which excludes food and energy—is likely to lag because it will take time for output gaps to close and activity to normalize.

Andy says that higher headline inflation data could spark a debate about whether EM central banks need to raise rates to help stem inflation, which has historically been a problem in many EMs. On balance, he thinks that most EM central banks will keep rates on hold this year unless they experience a substantial increase in longer-run core inflation. He notes that Brazil and the Czech Republic, which are already experiencing meaningful inflationary pressure, are potential exceptions where central banks could begin rate hiking cycles.

Higher Yields Reflect Supportive Economic Backdrop

So far, the Fed has been willing to look through the rising Treasury yields. Policymakers have not chosen to put downward pressure on long-term yields by changing the composition of the Fed’s quantitative easing purchases to focus on longer-maturity bonds. Chief International Economist Nikolaj Schmidt makes the case that the Fed is standing pat because the steepening yield curve simply reflects the supportive backdrop of economic reopening and aggressively expansionary fiscal stimulus.

Nikolaj also thinks that there may be a more subtle reason for the Fed’s inaction: Fed policymakers may be wary of creating a bond market bubble if they move to keep longer-term yields from reflecting the improving growth outlook. (Bond prices and yields move in opposite directions.) This would potentially increase the risk of a disorderly sell-off in bonds when the central bank eventually moves to taper its accommodative policies.

Diversity of Views

I believe that this diversity of perspectives on the implications of rising rates can give our active management approach an advantage in this highly unusual environment. The modern global economy had never experienced a downturn like that of 2020, and the extreme levels of fiscal and monetary stimulus provide the potential for an atypically fast recovery later in 2021. In my view, with this uncertain backdrop, this range of perspectives within T. Rowe Price should allow us to better navigate the possible market scenarios as the economic rebound evolves.

This range of perspectives can help portfolio managers evaluate the potential for scenarios that may not exactly align with their own outlook.

Key Risks—The following risks are materially relevant to the strategies highlighted in this material:

Growth stocks are subject to the volatility inherent in common stock investing, and their share price may fluctuate more than that of income-oriented stocks. The value approach to investing carries the risk that the market will not recognize a security’s intrinsic value for a long time or that a stock judged to be undervalued may actually be appropriately priced. Dividends are not guaranteed and are subject to change. International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. The risks of international investing are heightened for investments in emerging market and frontier market countries. Emerging and frontier market countries tend to have economic structures that are less diverse and mature, and political systems that are less stable, than those of developed market countries.

Debt securities could suffer an adverse change in financial condition due to a ratings downgrade or default, which may affect the value of an investment. Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest rate risk. As interest rates rise, bond prices generally fall. Investments in high-yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities. In periods of no or low inflation, other types of bonds, such as U.S. Treasury bonds, may perform better than Treasury inflation protected securities.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

March 2021 / INVESTMENT INSIGHTS

Rob Sharps is the chief executive officer and president of Price Group. He is the chair of the company’s Executive, Management, and Management Compensation and Development Committees.