June 2021 / INVESTMENT INSIGHTS

Four Keys to Tackling the Green Bond Boom

Increased issuance means more buy-side diligence is needed

Key Insights

- Green bonds, debt devoted to financing environmentally friendly projects, has been the cornerstone of environmental, social, and governance issuance’s growth over the last few years.

- The growth in the market has highlighted several problems, however, including a lack of uniform global standards, as well as the risk of “greenwashing.”

- As the market matures, we believe it will reward companies with ambitious and credible green frameworks.

The extraordinary growth of debt issuance with an environmental, social, and governance (ESG) focus over the last few years has brought responsible investing to the forefront of fixed income management, with the increase in issuance of “green” bonds—debt attached to environmentally conscious projects—being a major driving force behind this, in particular. The development of the market has provided a significant opportunity for managers, with access to a range of highly sought after, ecologically minded projects as well as new opportunities to find sources of yield.

The segment’s growing popularity, however, belies several unique challenges that managers face when addressing the green bond market. Despite appearing to carry a well‑established premium compared with vanilla bonds, for instance, the market as a whole lacks enforceable and concrete standards around criteria such as labeling and reporting. In addition, the wide spectrum of what constitutes “green” leaves the market open to greenwashing, with companies able to issue bonds certified green across very broad definitions. Governance problems, stemming from bonds being tied to projects rather than companies, is also an issue.

As the market grows, we are likely to see more events that will give managers pause for thought. In order to help navigate these pitfalls, investors should take a long‑term approach to their security selection on the conviction that, over time, we believe companies that showcase consistent commitment to green practices will be rewarded.

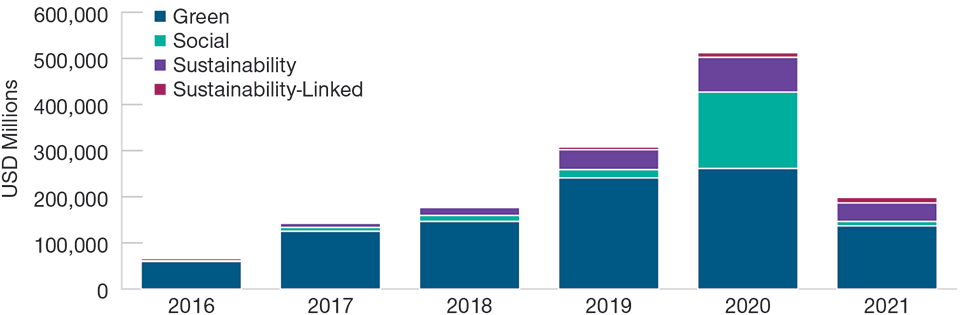

Green Bonds Have Historically Dominated ESG Issuance

(Fig. 1) First quarter 2021 green issuance almost outstripped the entirety of 2017

As of March 31, 2021.

Source: Bloomberg Finance L.P.

Green bonds are issues where proceeds are used to finance or refinance specifically climate‑related or environmental projects. Social bonds are issues where proceeds are used to finance or refinance projects specifically aimed at creating positive social outcomes in communities. Sustainability bonds are issues where proceeds are used to finance or refinance a combination of green and social projects or activities. Sustainability‑linked bonds are structurally linked to the issuer’s achievement of climate or broader sustainable development goals.

Green Bonds Driving ESG Debt Boom

Despite the need for job creation projects sparking a boom in social‑related issuance last year, green bonds have largely dominated the ESG space in recent times. In U.S. dollar terms, green bonds made up between 70% and 85% of total ESG‑related issuance each year from 2016 to 2019. And while social took the top spot last year, driven largely by securities issued under the European Union’s temporary Support to mitigate Unemployment Risks in an Emergency (SURE) program, an initiative to help member states combat the negative impact of the coronavirus pandemic, figures in the green space are still rising on an absolute basis. This year, more than USD 117 billion was issued in the first quarter alone. Considering that USD 120.9 billion in green bonds was issued in the entirety of 2017, the pathway for the asset class’s continued growth is apparent.

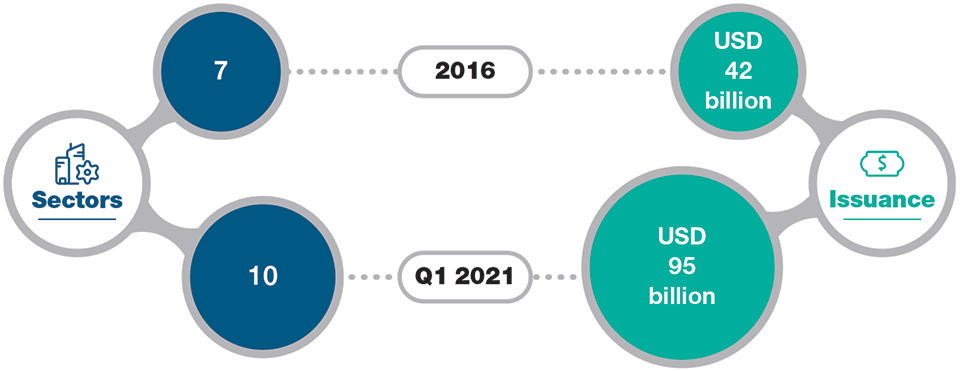

The increasingly diverse nature of the green bond market could also support its continued growth. Although financials, utilities, and sovereign issuance largely dominate the space, the rising number of issues from other sectors may be a sign of the maturation of the asset class. The first quarter of 2021 saw green bond issuance across 10 different corporate sectors in the period, a record number over the last five years, alongside rising dollar value. Recent high‑profile examples of new‑to‑market corporate issuers include Daimler, Volkswagen, and Volvo, which all issued inaugural green bonds within two months of each other in late 2020.

The rise of green bond issuance comes at a time when demand for ESG securities is insatiable. However, this perfect storm of booming supply and demand could come at a cost if investors are not careful. In particular, the complexity of what green bond issuers are bringing to market is often underrepresented, in our view, and could lead to some unwelcome surprises for investors down the line.

ESG Debt Requires Deeper Analysis

One risk some investors run is not applying an adequate level of diligence on the bonds, which can stem from two facets. On the one hand, as investor demand grows, so do their allocation allowances for green‑graded securities. Over time, this could create a dynamic where the set allocation is too large for a single investor to adequately scrutinize targeted credits. This could potentially lead investors to purchase “green‑washed” bonds—securities that are ESG labeled but are in fact issued for financial rather than environmentally friendly purposes.

Corporate Green Bond Issuance Is Growing and Diversifying

(Fig. 2) First quarter issuance outstripped the entirety of 2016

As of March 31, 2021.

Source: Bloomberg Finance L.P.

Away from dynamics, the analysis of the bond itself is also key, and, in particular, understanding that the bond is tied to a green project, not to the company. While on the surface this may appear immaterial, it could give rise to some form of cognitive dissonance between a firm’s climate‑friendly proposal and its business practices as a whole. For example, funding a project aimed at reducing carbon emissions may be an attractive proposition, but how much value does it really hold if the company behind it has seen total emissions rise year on year?

On a more practical level, failing to account for this separation between bond, project, and company can have dire consequences for investors. A recent example is the green bonds issued by the Mexico City Airport Trust to finance a new airport for the country’s capital in 2016 and 2017. The trust raised USD 6 billion, with the debt even earning green evaluations from Moody’s and S&P. However, in 2018, the newly elected Mexican government stopped construction at the airport. Green downgrades followed from the likes of Moody’s, however, the bonds still retain a green label, despite not funding an eligible green project.

Another example is RWE‑owned renewable energy firm Innogy, which issued a green bond in 2017. The EUR 850 million in proceeds from the issue was slated to be used to refinance five European wind farms. The following year, however, a deal struck by RWE and rival E.ON saw Innogy and most of its liabilities move to the latter; however, the wind farms remained under the auspices of RWE. Innogy’s proceeds were eventually reallocated to renewable grid projects, but regardless, the situation highlights how relatively easily green bond projects can become divorced from their financial home.

Standards Need Improving

The above is compounded by a lack of clarity and enforcement of standards on an international level. While levels of diligence and oversight do exist, including guidelines from the International Capital Market Association (ICMA), an expanded climate bonds initiative aligned with the Paris Agreement building on ICMA’s principles, and EU‑set standards and taxonomy on green bonds, these measures are still only voluntary. In addition, while sustainable ratings agencies do provide a degree of scrutiny, some charge fees to companies to provide an ESG rating, creating an inherent conflict of interest.

All of this is compounded by who labels a bond green in the first place; all ESG bonds, not just green, are self‑labeled, meaning that for a bond to be categorized as such, an issuer simply has to label it as so at issuance. While the existence of certain standards and ratings do alleviate some of the inherent risks around bonds declared green by their own issuers, we believe there is still a way to go before the market can have full faith in a set of enforceable rules and regulations governing green‑labeled securities.

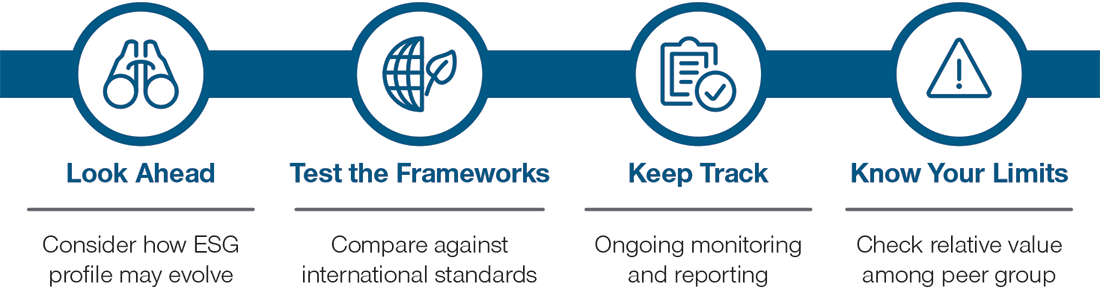

Guiderails for Entering the Green Bond Market

(Fig. 3) The sector’s complexities demand a long-term approach

Same Risk, Likely More Cost

Alongside these factors, investors also need to consider whether they are willing to pay the additional cost often associated with buying into green bonds rather than a vanilla equivalent. This so‑called greenium occurs despite the fact that, structurally, there isn’t a difference between an issuer’s green and non‑green bonds; on the surface, they each carry the same risk. This is visible in several markets but is particularly acute in the U.S., where green bonds with maturities longer than 10 years have priced, on average, around 10 basis points tighter than their non‑green equivalents. Given the issues we have outlined regarding the green label, this may be a cause for consternation among investors.

Looking Beyond the Green Bond Label

For investors, therefore, it’s vital to consider these factors when assessing points of entry into green bonds. The market can offer opportunity; however, a lack of investigation and preparation could lead to problems.

In our view, approaching the green bond space is about looking beyond the label, marrying fundamental research with a collaborative mindset. With this in mind, we believe the following are some of the main priorities to keep in mind when eyeing investments in environmentally focused debt.

Look ahead. Analyzing the ESG profile of a company at the present time is only half the battle. To help aid security selection, investors should aim to project how a company’s ESG profile is likely to evolve in the future, rather than how it exists in a vacuum.

Test the frameworks. Given the risk of greenwashing, it’s important to assess how an issuer’s own green bond frameworks line up with existing international standards to identify just how green a bond is. Opinions from second parties could also be sought.

Keep track. Ongoing monitoring and reporting after issuance can help ensure that companies follow through on their commitments. Analyzing the use of proceeds—from credibility and ambition at the roadshow through to the reality of usage as time passes—also helps to establish a company’s track record on how serious it is about ESG.

Know your limits. While going green is a focus, it is important to remember that hunting for relative value among a peer group is also key, particularly with the greenium typically making valuations even richer.

ESG‑conscious investing is now firmly embedded in the fixed income space. While the rise of green bonds does testify to this, the overwhelming supply and demand dynamics have created an environment that can be exploited by issuers looking to undermine the noble aims of climate‑conscious investing. However, we believe the market will, in the long term, reward issuers who present credible and ambitious green frameworks, and investors should have this in mind when selecting securities.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

June 2021 / WEBINAR