June 2021 / INVESTMENT INSIGHTS

Are Tight Credit Valuations Justified?

Positive tailwinds are providing support, but caution is advised

Key Insights

- The strong macro environment is providing support for credit markets, but valuations are compressed.

- At current spread levels, we are casting the net wider to find interesting opportunities in assets such as convertible bonds.

- Over the medium term, we are cautious and watching economic data closely for signs that the recovery is sustainable.

Credit markets have been remarkably resilient so far in 2021, with spreads tightening even as a fierce sell‑off raged across developed government bonds. In our latest investment team meetings, we discussed the dynamics driving credit markets and whether they will continue.

Global Growth Recovery Supports Credit

The stars have aligned for credit markets this year, with positive tailwinds coming from ultra-accommodative monetary policy, expansionary fiscal policy, and improving economic growth. These powerful forces have helped to drive credit spreads in sectors such as U.S. high yield to multiyear tights, leaving many investors questioning how much longer this move has to run.

“There is no reason to panic yet—credit spreads don’t tend to sell off because of tight valuations, but rather because of a change in the macro environment,” said Saurabh Sud, a portfolio manager and member of the fixed income global investment team. Such a change is unlikely to occur over the next few months because economic growth is expected to continue its strong recovery as vaccines are rolled out and restrictions are eased, Mr. Sud added.

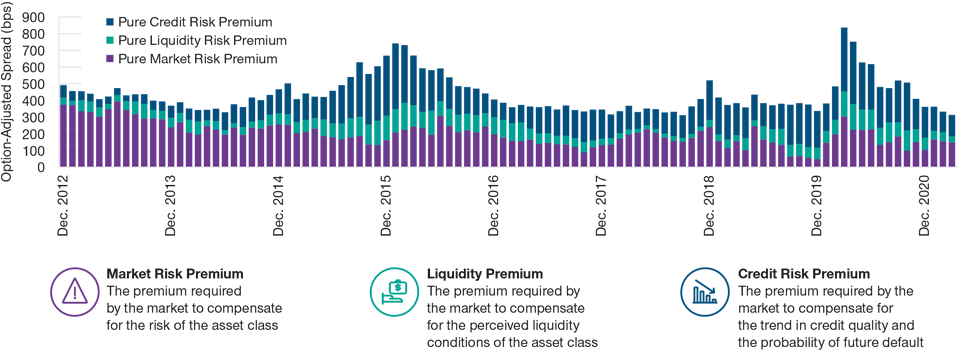

Analyzing the premium that investors demand to hold corporate bonds could also provide useful information for what might happen next. Let’s remind ourselves that credit premia can be decomposed into three parts: a pure liquidity component, a pure credit quality component, and a pure market risk component. Given the extraordinary amount of ongoing monetary and fiscal policy support, it could be argued that the liquidity and credit components are likely to remain stable or potentially even compress a bit further from here. Although the market risk premium could increase if there is an unexpected spike in volatility. On the other hand, market technicals are incrementally less positive due to higher supply, as are fundamentals given increased mergers and acquisitions activity and shareholder‑friendly actions.

(Fig. 1) Credit Premium Breakdown

Decomposition of U.S. high yield credit premium

As of March 31, 2021.

Past performance is not a reliable indicator of future performance.

For illustrative purposes only.

T. Rowe Price spread decomposition calculation is based on default rates, liquidity indicators such as bid and ask prices, and volatility of index components.

Source: Bloomberg Barclays U.S. High Yield Bond Index. Analysis by T. Rowe Price (see Additional Disclosure).

Taking all these factors into account, allocations to credit markets still make sense, but we believe that some caution and greater selectivity are warranted given the tightness of spreads. “The risk/reward from holding credit has waned since the start of the year,” said Mr. Sud. He noted that this has led T. Rowe Price to reduce credit exposure in some of our strategies, although he retains a broadly positive bias.

Finding Opportunities in Convertible Bonds

In the current market environment, we have a preference for shorter maturities, greater liquidity, and credits dislocated from fundamentals. In particular, we favor bonds from sectors that have suffered during the pandemic and could potentially be key beneficiaries of economies recovering, such as banking. Liquidity is also important, and in this regard we favor derivative instruments and select names in the technology, media, and telecom sectors that should benefit from regular revenue streams.

The new issuance market is another area to monitor for potential opportunities. There are more complex credit stories starting to come through particularly in European high yield. While these may carry higher risk, they also may offer good long-term value potential; however, credit-intensive research is required to try to identify the successful stories and, just as importantly, the companies to be avoided.

Casting the net wider to find value is also important. “At current spread levels, we have been spending time uncovering opportunities further afield such as in convertible bonds,” said Mr. Sud. Here, we have partnered with our equity and fixed income research analysts to find some convertible debt that potentially offers more appealing upside convexity than the generic standalone bond.

Growth and Inflation Data Key Signposts for Market Direction

There appears to be little that could derail investor sentiment toward credit in the near term. Over the medium term, however, there are key risk factors that should be monitored. “Watching economic data will be particularly important as we need to see signs the recovery is sustainable beyond the second quarter when growth, stimulus, and reopening optimism are all expected to peak,” said Mr. Sud. He warned that this year’s fiscal stimulus tailwind, for example, will likely turn into a headwind in 2022 as spending is reduced and taxes potentially are increased.

If strong economic data are maintained, there is a risk that real inflation pressures will start to build. Under this scenario, the resolve of central banks such as the Federal Reserve to remain accommodative could be tested. “Any signs that the Fed is changing course and moving toward tightening could drive core bond yields another leg higher and negatively impact investor risk sentiment,” noted Mr. Sud. It is unlikely that credit would escape unscathed in that situation, again underlining the importance of watching economic data.

The equity market could also offer helpful insights into the future behavior of credit spreads, particularly the ratio of U.S. large‑cap cyclical performance to defensives. In the past, new lows in this index have often been a precursor for credit spreads widening. At present, the ratio remains on an upward trajectory—but if that were to reverse, it may be a sign for caution. We are monitoring the situation closely.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

Arif Husain is the head of Global Fixed Income and chief investment officer of the Fixed Income Division. He is chairman of the Fixed Income Steering Committee and a member of the firm’s Management Committee. Arif is lead portfolio manager for the Global Government Bond High Quality Strategy. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.