April 2023 / RETIREMENT INSIGHTS

Reference Point: Annual Recordkeeping Report

Reference Point 2023 provides data and actionable insights into plan and participant activity throughout the year. This valuable benchmarking tool analyzes key trends and shares expert commentary you can use to inform your plan strategy decisions.

Report highlights

The year 2022 started with market volatility caused by war, dealt out significant inflation and fears of recession, and ended with one of the most substantial pieces of retirement legislation in years. It’s enough change to unsettle even the most prepared retirement savers. While most retirement savers stayed the course, we did see some changes as a result of 2022’s economic challenges:

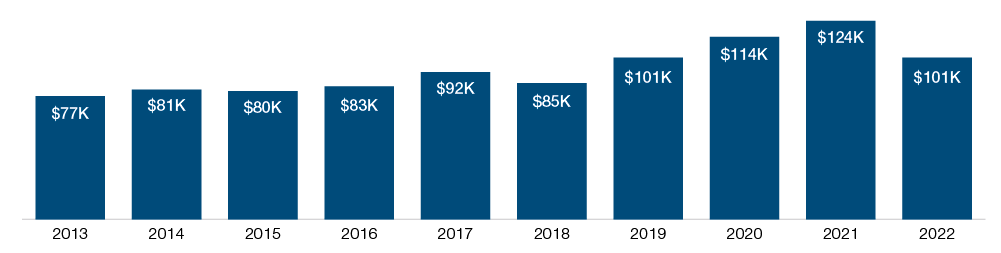

- The average account balance dropped from $124K in 2021 to $101K in 2022, which was a decrease of 18% compared with the 20% drop experienced by the S&P 500 Index.

- The average combined employee deferral rate declined slightly from 8.5% to 8.4%.

- Allocations to stock funds decreased from 34.8% in 2021 to 31.7% in 2022.

- Allocations to money market and stable value increased from 7.5% in 2021 to 9.6% in 2022.

- While loan usage remained below the pre-pandemic average (18.3% of participants had a loan in 2022 compared with 18.5% in 2021 and 22.1% in 2019), average loan size has grown 17% since 2013 and reached a 10-year high of $9,837 in 2022.

Average account balances

Plan design is helping

For years, retirement plans have proven that auto-solutions are effective plan design features to get participants enrolled, saving, and investing. This was apparent in 2022, even as market and economic uncertainties threatened to push participants off track.

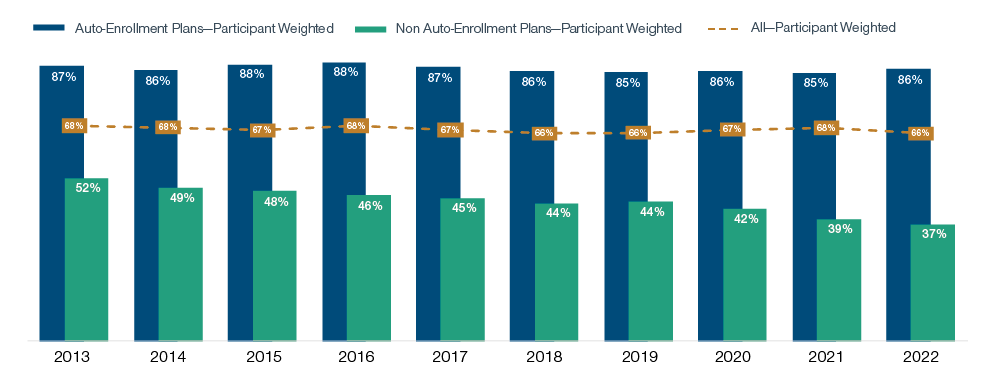

Plan adoption of auto-enrollment rose in 2022 to 85%, continuing an eight-year trend. Overall participant-weighted participation rates fell from 68% in 2021 to 66% in 2022. But despite the declines, auto-enrollment continued to yield far higher participation rates: 86% in 2022 compared with just 37% for plans without auto-enrollment.

Participation rate: Auto-enrollment vs. non-auto-enrollment

How will SECURE 2.0 affect trends moving forward?

The SECURE 2.0 Act of 2022 introduces mandatory and optional provisions that will help increase coverage and allow participants to save more and longer for retirement. The law also helps sponsors to tailor their plans more specifically to the needs of their plan population.

How it will affect plan and participant trends is yet to be seen, given that many of the provisions will not go into effect until 2024, 2025, and beyond. We do anticipate that plan sponsors might implement new plan design features or make other changes based on SECURE 2.0, specifically in these areas:

- Auto-enrollment and auto-increase: New plans will be required to offer the two features, effective in 2025. While this provision applies only to new plans, plan sponsors might add or modify the auto-solutions in their existing plans.

- Roth: Starting in 2024, all catch-up contributions will be required to occur on a Roth basis for participants earning more than $145,000 in prior-year wages from the employer sponsoring the plan. This provision may substantially affect trends, as plans adopt Roth for the first time and more participants start contributing on a Roth basis. Beginning in 2024, RMDs are not required from Roth accounts in a plan, so there would be no need to roll over to an IRA to avoid RMDs.

- Student loan match and emergency savings: We expect that the retirement industry and employers will be tracking trends related to retirement plan matching contributions of student loan payments and emergency savings distributions with the financial wellness provisions included in SECURE 2.0.

About the Report

Unless otherwise noted, all data included in this report are drawn from the following sources: Data are based on the large-market, full-service universe—T. Rowe Price total—of T. Rowe Price Retirement Plan Services, Inc., retirement plans (401(k) and 457 plans) consisting of 652 plans and approximately 2 million participants.

For more information on this report or where you can get additional industry-specific data to support your plan design discussions, please contact your T. Rowe Price representative.

This material is provided for general and educational purposes only and is not intended to provide legal, tax, or investment advice. This material does not provide recommendations concerning investments, investment strategies, or account types; it is not intended to suggest that any particular investment action is appropriate for you. Please consider your own circumstances before making an investment decision.

IMPORTANT INFORMATION

This material is provided for general and educational purposes only and is not intended to provide legal, tax, or investment advice. This material does not provide recommendations concerning investments, investment strategies, or account types; it is not individualized to the needs of any specific investor and not intended to suggest any particular investment action is appropriate for you, nor is it intended to serve as the primary basis for investment decision making.

The views contained herein are those of the authors as of March 2022 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

Study results provided throughout the material are as of the most recent date available and are subject to change.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Associates, Inc., T. Rowe Price Investment Services, Inc., T. Rowe Price Retirement Plan Services, Inc.

©2023 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, RETIRE WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

April 2023 / GLOBAL FIXED INCOME