February 2023 / INVESTMENT INSIGHTS

The Energy Crisis Is Only Just Beginning

Next winter is where the real challenge lies.

Key Insights

- Transitioning away from Russian gas will be a major challenge in 2023 as countries struggle to find and process enough imported liquefied natural gas to meet the shortfall.

- Renewable energy is the long‑term solution, but the infrastructure does not yet exist for renewables to replace fossil fuels.

- We believe the scramble to obtain enough fossil fuels to meet short‑term demand will lead to higher energy bills and a likely recession.

Wholesale gas prices surged in the summer of 2022, leading to dire predictions of blackouts, rationing, and people freezing in their homes. Since then, prices have retraced as it has become clear that most European countries have largely succeeded in filling their gas storage facilities ahead of the winter. It would be a mistake to assume the energy crisis is over though—in many ways, it is only just beginning.

After the invasion of Ukraine, Russian President Vladimir Putin sought to use Russia’s vast oil and gas reserves as a tool to weaken opposition among western countries. Given the dependence of Germany, Italy, and other European countries on cheap Russian energy, there were concerns that standing up to Russia would inflict more economic and social damage than the continent could stand.

But the threat of turning off the gas was a weapon that Putin could only fire once. As the threat became clear, countries began scrambling to find alternative sources of energy. Since the invasion, gas imports from Russia to European Union (EU) countries have fallen significantly, largely offset by a sharp increase in imports of liquefied natural gas (LNG) from the U.S. and Qatar. At one point, there were so many LNG tankers queuing up at European ports that gas spot prices briefly went negative.

At the same time, European countries have announced energy price caps to protect people and businesses from the fallout of the energy crisis. These expensive programs have fueled government borrowing but have helped to prevent social instability and sharp economic contraction. Gas consumption has also fallen significantly as a result of soaring prices, warmer weather, and demand destruction in the industrial sector.

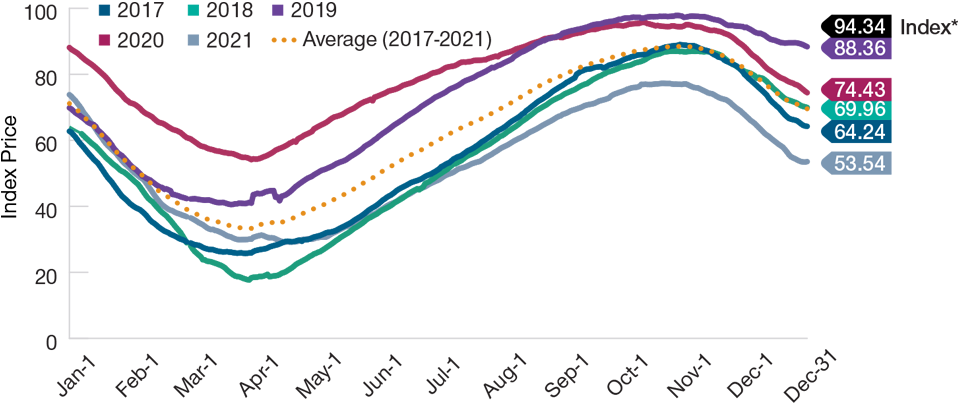

Gas Storage Facilities in Europe Are Largely Full

(Fig. 1) The continent is well placed to navigate the winter

As of December 7, 2022.

*Europe % Gas Full Index (last price available, December 7, 2022).

Source: Bloomberg Finance L.P.

Gas storage facilities in Europe are well stocked compared with previous years (Figure 1) and, based on the current rate of demand, the continent is likely to head into spring 2023 with 30 billion cubic meters (bcm) to 50bcm of storage remaining—a much better position than could have been imagined just a few months ago. This means that Europe is unlikely to face a major energy crisis this winter unless there is a spike in demand due to cold weather or a reversal of demand destruction patterns.

It is far too soon to declare victory in the energy war, however. Although Putin’s attempt to use Europe’s dependence on Russian gas as a blackmail tool has failed, Europe still faces a major challenge in ensuring its energy needs are met in the winter of 2023 to 2024 and beyond. The era of Russia acting as a major supplier of Europe’s energy needs is over—there is no going back to the pre‑Ukraine war status quo. Russia would not have sabotaged its Nord Stream pipelines to Germany if it was considering sending gas to Europe again—and even if it were, there is no appetite in Europe to become dependent on Russian energy again. Europe’s future energy needs will need to be met in other ways.

Transitioning away from Russian energy will not be easy, however. Despite the fall in energy imports from Russia since the invasion, Russia still accounts for more than 40% of Europe’s stored gas for this winter. Put simply, if Europe has around 50bcm of gas storage left next spring, it will need to attract a very large quantity of LNG again to make it safely through to spring 2024. At current levels of demand, this would mean that Europe would need to attract 30% of the global LNG market, or 35% of the global spot market once already‑contracted volumes are stripped out.

This may be a tall order. There was a 12% increase in LNG imports to Europe from the U.S. in 2022, but this rate of growth cannot be sustained because U.S. production and export capacity is currently at a maximum. Even if more U.S. exports were available, there is currently limited capacity in Europe to process LNG imports. While there are plans to build new LNG‑processing infrastructure in Europe, this will likely take several years to complete.

What’s more, much of the LNG imported to Europe in 2022 came from Russia, which will not be possible in 2023 due to sanctions. Global demand for LNG is also likely to rise in 2023, particularly as China has begun to loosen its “zero‑COVID” policies. LNG is already very expensive, and prices will likely increase in 2023 as demand increases.

In the long term, renewables will replace Russian imports as a key supplier of Europe’s energy needs, but this prospect is some years away. Planning, funding, and building wind and solar farms is a multiyear process. Installing the pipes and other infrastructure to enable households and businesses to use wind and solar power may take even longer. Supplies of wind turbines and solar panels are also limited because of bottlenecks arising from China’s COVID lockdown policies, as well as delays in permissioning and financing. Renewable energy is the future but not the only solution to Europe’s energy requirements in the immediate future.

Which means that fossil fuels will continue to play a vital role for some time to come. The short‑term story is therefore one of elevated prices and heightened volatility as countries scramble to identify alternative sources of gas. This will come at a huge cost as governments deal with rising prices while simultaneously subsidizing their populations’ energy bills. If countries struggle to source all the gas they need, consumption may have to be cut—but persuading people to use less gas and electricity will not be easy.

We believe that many European and other countries face a recession this year, largely caused by the energy crisis. It is clear, then, that Russia’s invasion of Ukraine will continue to reverberate through energy markets for an extended period. The threat to turn off the gas pipes may have been a weapon that Russia could only fire once, but its macroeconomic impact will be felt for years to come.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

February 2023 / INVESTMENT INSIGHTS

Justin Thomson is the head of International Equity. Justin is a member of the Management Committee and the chairman of the International Equity Steering Committee. He is a member of the Asset Allocation and ESG Committees. He also is the chief investment officer for International Equities. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.