May 2023 / ASSET ALLOCATION

Is the Employment Picture Turning?

The U.S. labor market faces headwinds amid tighter credit conditions for small businesses and declining corporate profit margins.

Key Insights

- The U.S. labor market faces headwinds amid tighter credit conditions for small businesses and declining corporate profit margins.

- We are closely monitoring forward-looking employment indicators, as historical data show that a persistent uptick in unemployment can be difficult to reverse.

Transcript

Employment is a key recession indicator. In the first and second quarters of 2022, real GDP growth was negative. While two consecutive quarters of negative GDP growth would typically constitute a recession, this period was not officially considered a recession primarily because employment did not weaken.

In fact, employment actually improved during both quarters with the unemployment rate falling from 3.9% as of December 2021 to 3.6% as of June 2022. And despite further economic softness over the past year, the unemployment rate has improved further and remains at a remarkably low level of 3.5% as of March 2023.

On top of this low unemployment rate, there are also almost 10 million unfilled job openings in the U.S. economy based on the March 2023 jobs report. Which means there are approximately 1.7 job openings for every single unemployed worker, a historically strong level for the labor market.

However, there are reasons to be concerned that the strength of the labor market could rapidly evaporate over the next 12 months.

Small Businesses

One reason to be concerned is the role that small businesses play in the employment market.

Small businesses account for a very large share of U.S. employment. According to the U.S. Department of Labor statistics as of March 2022, businesses with less than 250 employees accounted for 73% of all jobs in the U.S.

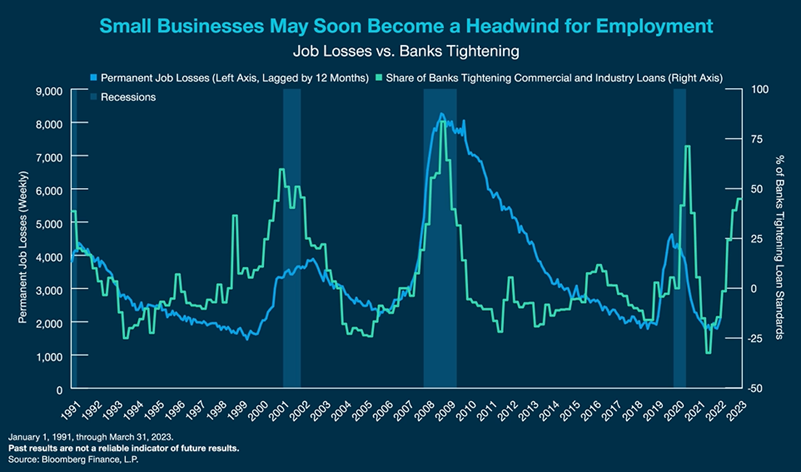

The reason this is concerning is because small businesses rely heavily on banks for their ongoing credit needs. This means that when banks become more cautious about offering loans to business clients, small business activity usually suffers and consequently the job market tends to weaken. We can illustrate this relationship by comparing historical data on bank lending standards to data on job losses over the subsequent 12 months.

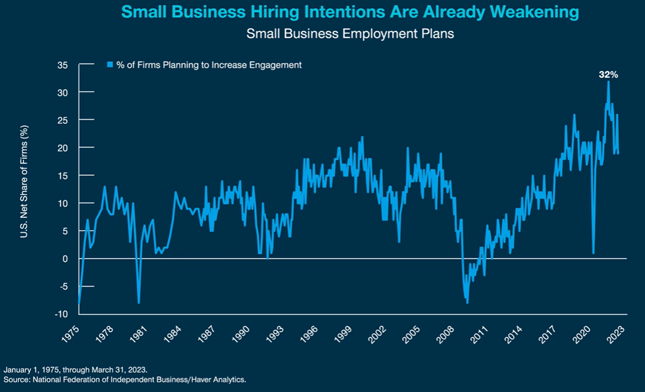

Given that bank lending standards have already tightened considerably, a sharp increase in job losses could potentially be on the horizon. In fact, economic survey data tell us that hiring intentions at small businesses are already weakening, albeit from a very strong level.

Corporate Profit Margins

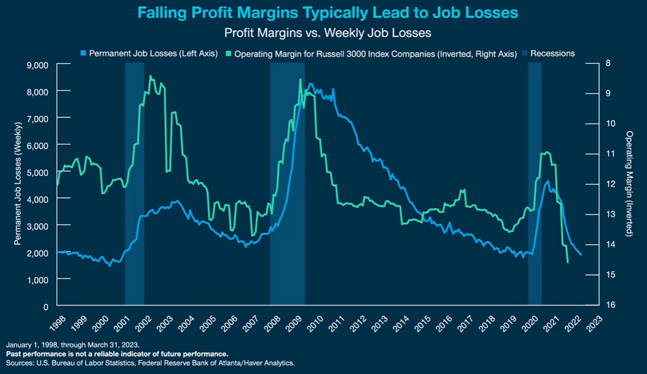

Another reason for concern is that corporate profit margins are falling. When input costs spiked in 2021 and 2022, corporations were initially able to pass these higher costs on to consumers in the form of higher prices. But consumers have become much less willing to pay higher prices as their savings balances have dwindled.

As a result, corporate profit margins have begun to come under pressure—and while they remain at relatively healthy levels in aggregate, those businesses that already had narrow margins are beginning to see profit margins go negative.

Unfortunately, falling profit margins are almost always bad news for employment, as once employers begin losing money they are inevitably forced to cut costs by laying off employees.

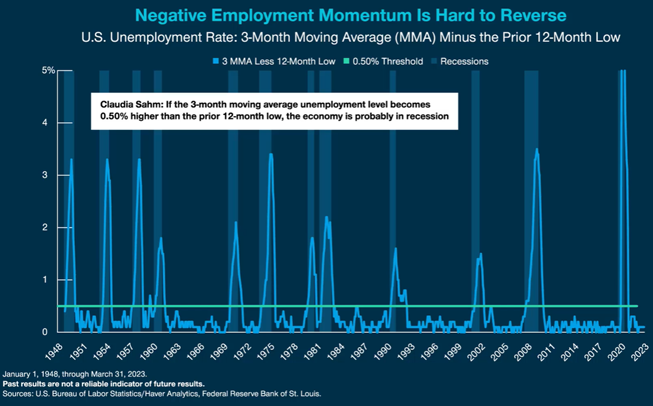

Negative Momentum Is Hard to Reverse

The good news is that we are still in the very early stages of the employment market weakening. In fact, a modest amount of weakness in employment could help push wage inflation back to sustainable levels, which is exactly what the Fed is trying to achieve by raising interest rates.

Unfortunately, history tells us that weakening employment a little, but not a lot, is very difficult to achieve. This was famously captured by former Fed economist Claudia Sahm, who observed that whenever the three-month moving average of the national unemployment rate has risen by 0.5 percentage points above its prior 12-month low, a recession has occurred. More simply put, once unemployment gains momentum, it is very hard to reverse.

Conclusion

In conclusion, the apparent strength of the U.S. employment market may be more tenuous than it appears. Forward-looking indicators are showing early signs of weakness, and history tells us that once employment momentum turns negative, it is hard to stop.

As a result, we remain cautious about the medium-term path for the U.S. economy and will be keeping a close eye on forward-looking employment indicators.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Tim Murray is a capital market strategist in the Multi-Asset Division. Tim is a vice president of T. Rowe Price Associates, Inc.