- On Retirement

- Plan Sponsor, Plan Sponsor, Make Me a Match

- Savings behavior impacts glide paths more than DC match formulas.

- 2022-02-04 04:03

- Key Insights

-

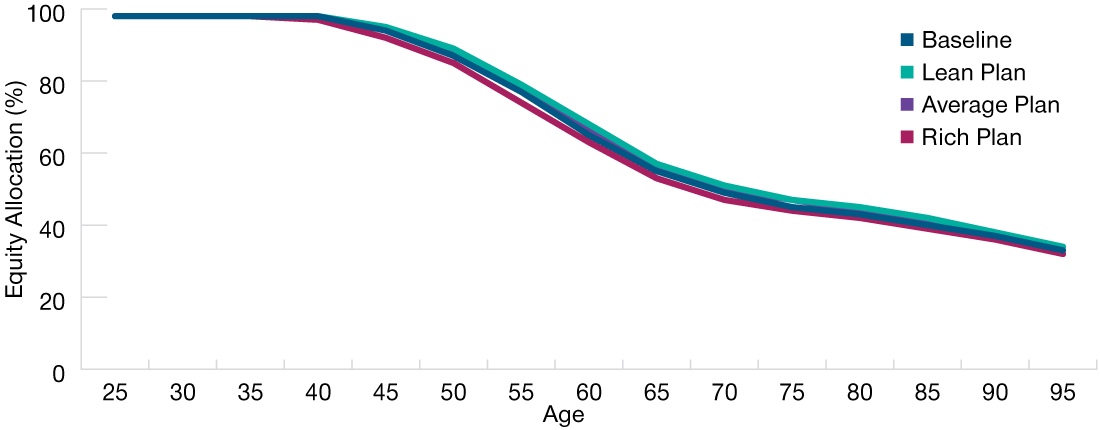

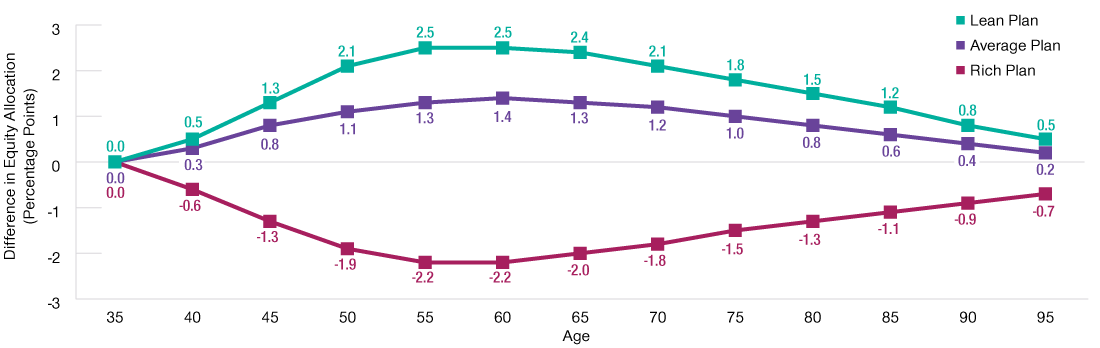

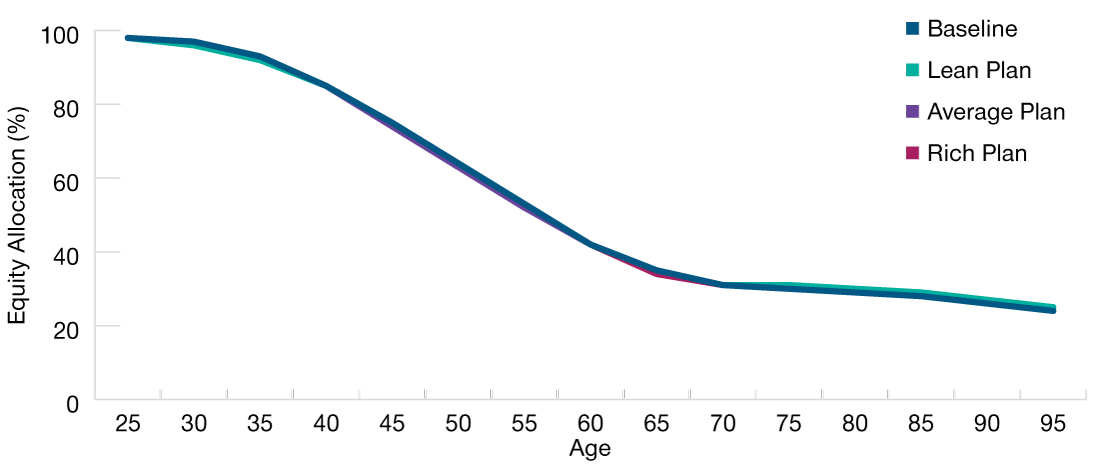

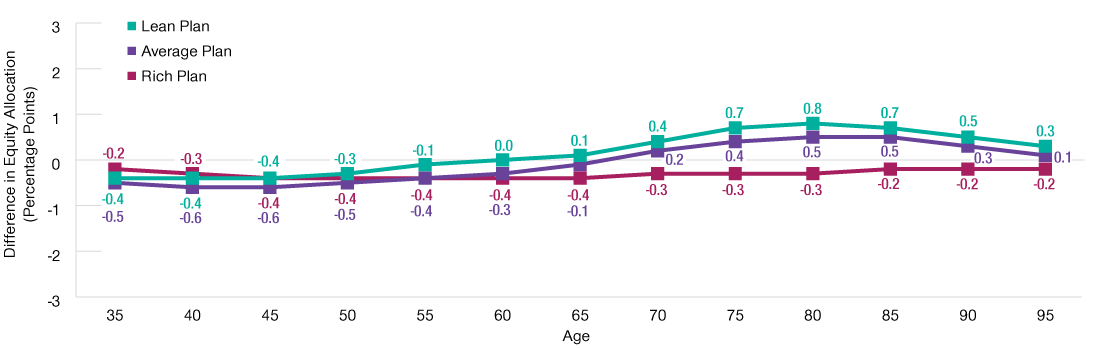

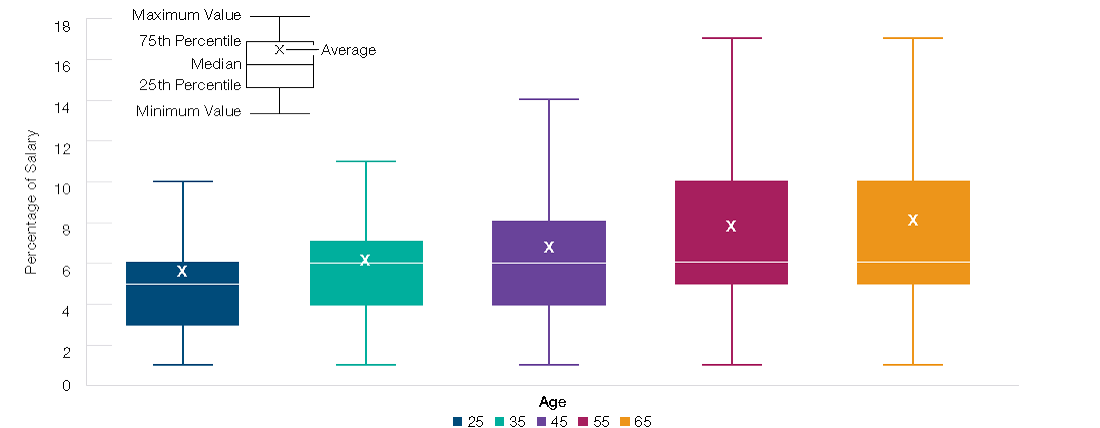

- Our modeling work found that participant savings behavior had a greater impact on glide path design than employer match generosity did.

- The richness of the match formula shifted the optimal glide path equity allocation by less than 5% at all ages, even in the absence of a defined benefit plan.

- These findings support the idea that participants ultimately own their outcomes when their retirements are supported primarily by defined contribution plans.

-

1 Justin Harvey and Adam Langer. “The Importance of Defined Benefit Plan Design” (2021). The impact of pairing various DB plan designs with an existing DC plan varied the optimal equity level in the glide path by as much as 31 percentage points in the designs we modeled. We also found that DB plan eligibility and the amount of wealth provided by that plan both needed to be considered when evaluating glide paths.

2 For the details of our modeling methodology, please see the Appendix.

3 Assuming employee deferral levels are held constant for all match formulas.

4 The combination of employer matching contributions and participant deferrals brought total savings closer to the 15% of salary that we believe is appropriate for most participants. See Judith Ward. “Reasons Why You Should Aim to Save 15% for Retirement” (2021), and Roger Young. “You’re Age 35, 50, or 60: How Much Should You Have Saved for Retirement by Now?” (2021).

5 Joshua Dietch and Taha Choukhmane. “Auto‑enrollment’s Long‑Term Effect on Retirement Saving” (2019).

-

Additional Disclosure

Monte Carlo simulations model future uncertainty. In contrast to tools generating average outcomes, Monte Carlo analyses produce outcome ranges based on probability—thus incorporating future uncertainty.

Material Assumptions include:

- Underlying economic and behavioral inputs, including savings rates and cash flows, are generated from a structural model built up from factors relating to both financial markets and the broad economy as well as data calibrated based on T. Rowe Price’s recordkeeping platform’s participant population.

- The mortality weighting is sourced from the Society of Actuaries. Retirement age is assumed to be 65 years old.

Material Limitations include:

- The analysis relies on assumptions, combined with a return model that generates a wide range of possible return scenarios from these assumptions. Despite our best efforts, there is no certainty that the assumptions and the model will accurately predict asset class return ranges going forward. As a consequence, the results of the analysis should be viewed as approximations, and users should allow a margin for error and not place too much reliance on the apparent precision of the results.

- Users should also keep in mind that seemingly small changes in input parameters, including the initial values for the underlying factors, may have a significant impact on results, and this (as well as mere passage of time) may lead to considerable variation in results for repeat users.

- Extreme market movements may occur more often than in the model.

- Market crises can cause asset classes to perform similarly, lowering the accuracy of our projected return assumptions, and diminishing the benefits of diversification (that is, of using many different asset classes) in ways not captured by the analysis. As a result, returns actually experienced by the investor may be more volatile than projected in our analysis.

- Asset class dynamics, including, but not limited to, risk, return, and the duration of “bull” and “bear” markets, can differ than those in the modeled scenarios.

- The analysis does not use all asset classes. Other asset classes may be similar or superior to those used.

- Fees and transaction costs are not taken into account.

- The analysis models asset classes, not investment products. As a result, the actual experience of an investor in a given investment product may differ from the range of projections generated by the simulation, even if the broad asset allocation of the investment product is similar to the one being modeled. Possible reasons for divergence include, but are not limited to, active management by the manager of the investment product. Active management for any particular investment product—the selection of a portfolio of individual securities that differs from the broad asset classes modeled in this analysis—can lead to the investment product having higher or lower returns than the range of projections in this analysis.

Modeling Assumptions:

- The primary asset classes used for this analysis are stocks and bonds. An effectively diversified portfolio theoretically involves all investable asset classes including stocks, bonds, real estate, foreign investments, commodities, precious metals, currencies, and others. Since it is unlikely that investors will own all of these assets, we selected the ones we believed to be the most appropriate for long-term investors.

- The analysis includes 10,000 scenarios. Withdrawals are made annually at the beginning of each year.

- IMPORTANT: The projections or other information generated by T. Rowe Price regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. The simulations are based on assumptions. There can be no assurance that the projected or simulated results will be achieved or sustained. The charts present only a range of possible outcomes. Actual results will vary with each use and over time, and such results may be better or worse than the simulated scenarios. Clients should be aware that the potential for loss (or gain) may be greater than demonstrated in the simulations.

- The results are not predictions, but they should be viewed as reasonable estimates.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. This material does not provide fiduciary recommendations concerning investments or investment management.

The views contained herein are those of the authors as of February 2022 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc., distributor, and T. Rowe Price Associates, Inc., investment advisor. For Institutional Investors Only.

© 2022 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.