- On Fixed Income

- Controlled Deflation of the China Property Debt Balloon

- Beijing’s policy actions in the property sector seem to be containing any potential contagion effect.

- 2021-09-27 15:03

- Key Insights

-

- We are confident that there will be a well‑managed deflation of the debt balloon in the real estate sector and that Evergrande’s troubles are unlikely to cause systemic risk.

- As the government looks to carefully manage economic and social impacts, we do not anticipate policy action in the real estate sector to amplify further.

- Volatility in the markets may present attractive opportunities in the sector.

What Is Happening With Evergrande?

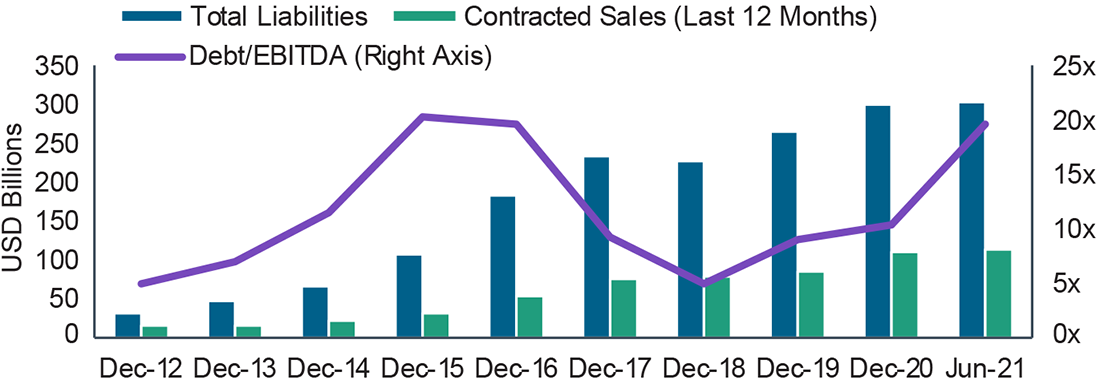

Evergrande is the second‑largest property developer in China by contracted sales (USD 111 billion in 2020). It has a 5% market share in the sector, which, together with the supply chain, composes over a quarter of economic activity in China. The company has undergone aggressive debt‑funded growth in the past few years as the sector grew rapidly, with urbanization remaining a focus in Beijing’s five‑year plans. As of June 2021, Evergrande had a total liability of more than USD 300 billion, almost triple what it had at the end of 2015.

Over the past few months, Evergrande’s financial situation has worsened. To avoid a disorderly default and contain the impact, Chinese regulators have moved to centralize all lawsuits against the company at the Guangzhou Intermediate Court.

China Evergrande’s Key Debt Metrics

(Fig. 1) Debt and liabilities have risen over the years

As of June 30, 2021.

For illustrative purposes only. EBITDA = Earnings Before Interest, Taxes, Depreciation and Amortization. This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services.

Source: Data from China Evergrande Group.

Policy Backdrop: Spread Widening

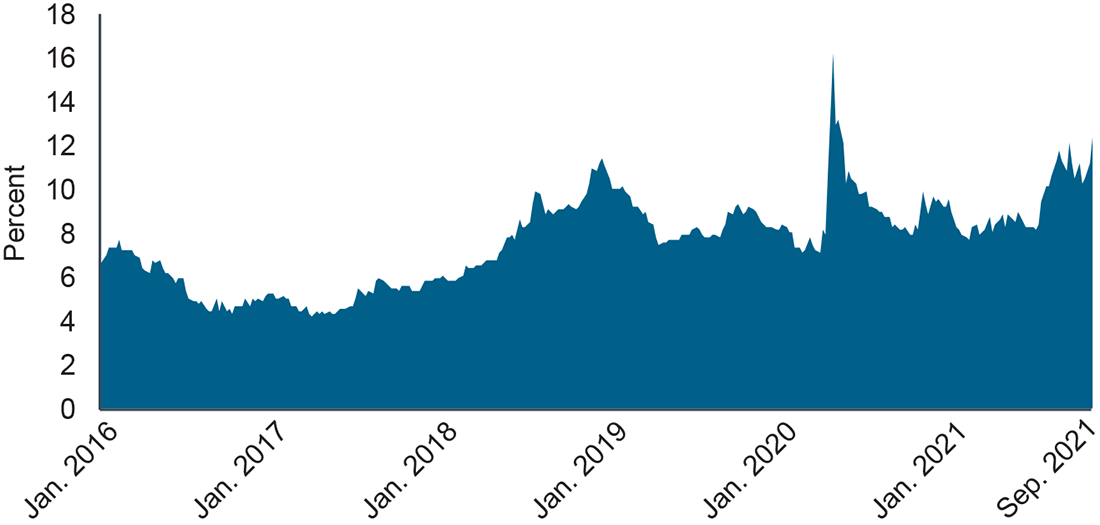

China real estate credit spreads1 have widened since the government started to tighten policies for the sector last year, with measures such as the introduction of the “three red lines” for developers and “two red lines” for banks.

The three red lines policy dictates the cash to short‑term debt, liability to asset (excluding contract liability), and net gearing ratios that property companies must achieve by 2023. It signals Beijing’s intent to inject greater discipline into the sector. Similarly, the two red lines policy for banks is aimed at capping mortgage lending and overall property‑related loans. While the intention is to help ensure the long‑term healthy development of the property sector, banks have been prudently reviewing their lending to the sector, which has contributed to tighter onshore financing channels for developers.

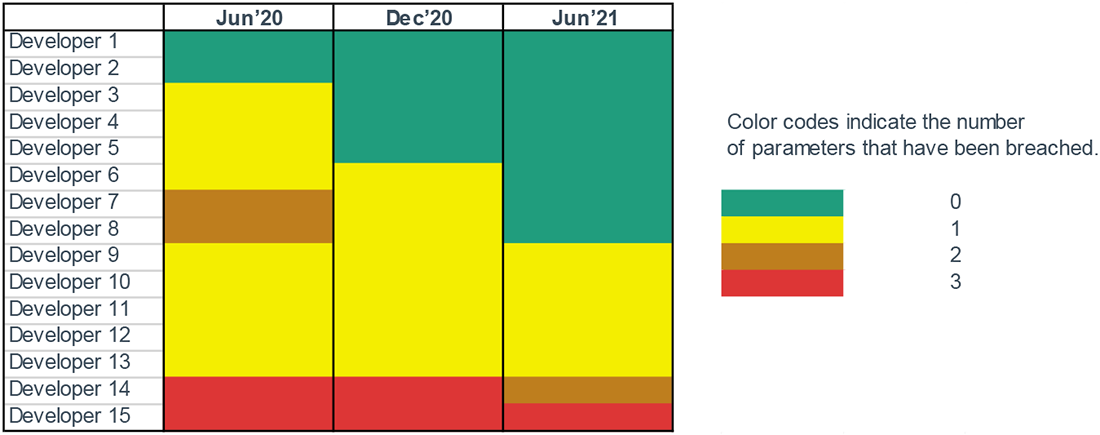

The three red lines policy has been particularly effective in curbing some of the more aggressive growth strategies among the developers. Year to date, the industry has become more prudent with land banking activity (acquiring land for future development), with average land purchases declining to 24% of contracted sales in the first half of 2021 from 39% in 2019 (and 34% in 2020). We have started to see improvements across the board since the three red lines policy was first unveiled, with several names in a list of China’s leading developers performing better on key metrics tracked by policymakers. (See Fig 3.)

USD High Yield China Real Estate Bond Yields Have Risen

(Fig. 2) Offshore investors turn cautious as financing channels narrow

As of September 17, 2021.

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Finance L.P./J.P. Morgan Chase (see Additional Disclosure), analysis by T. Rowe Price.

The Implications of Government Policy Action

We do not believe that a default by Evergrande will cause systemic risk in China’s credit markets.

We believe that there will be a well‑managed deflation of the debt balloon and that the current turbulence is unlikely to pose a test of financial stability in China. Although one of the larger developers, Evergrande accounts for a small amount of total sales in a fragmented industry. We expect that any impact to the banking system will be manageable and that the government will instead focus on the social fallout of unfinished housing units, followed by property supply chain suppliers exposed to Evergrande payables. Evergrande’s offshore USD bonds are currently trading at around 20‑30 cents on the dollar,2 but this reflects their lower ranking in claims. We expect onshore debt and liabilities will have priority in any debt restructuring process, and regulators are watching these closely to help ensure an orderly process.

"We believe that there will be a well‑managed deflation of the debt balloon and that the current turbulence is unlikely to pose a test of financial stability in China."

— Sheldon Chan, Fixed Income Portfolio Manager

"Policymakers will also be mindful of the potential social and economic impact."

— Sheldon Chan, Fixed Income Portfolio Manager

Policymakers will also be mindful of the potential social and economic impact. It is worth remembering that the implementation of policies in the property sector has historically moved in cycles, starting with actions that initially led to negative market reactions and hits to confidence, followed by efforts to stabilize sentiment.

Policy Impact on Selected Major China Property Developers

(Fig. 3) Fewer breaches of government‑tracked metrics over time

As of June 30, 2021.

For illustrative purposes only.

Source: Data from individual companies.

Policy toward the real estate sector is unlikely to be amplified further.

Physical market indicators such as average sales price, land sales, and new housing starts have all moderated recently, indicating some degree of policy success. China’s National Bureau of Statistics recently commented that the property curbs have contained unreasonable demand while at the same time warned that contagion impacts on the real estate industry need to be monitored closely. Our view is consistent with our conversations with management teams of the larger developers as well as industry consultants, where it is generally believed that we have seen the peak of policy tightening.

That said, we do not expect any material loosening of property policy in the near term. As part of the government’s strategy to structurally reduce risk in the broader financial system, the three red lines and two red lines policies were introduced as multiyear initiatives that are due to be “tested” in 2023 and 2024.

We expect the Asia high yield market to continue to differentiate among the different developers.

Under the three red lines, the trend of consolidation and divergence will likely continue. In 2016–2018, mainly large developers gained market share. The top 50 developers’ market share collectively grew from 36% in 2016 to 51% in 2018, remaining largely stable since. As regulators are determined to achieve their policy goals, developers with stronger execution and financial management should gain market share, with more stressed players exiting the market. Regardless of the overall monetary policy of China, funding available to the residential property sector will be closely controlled. Those that are unable to meet the three red lines requirement will suffer the most in a tight funding environment. Therefore, more defaults are possible in the near future.

-

1 Credit spreads measure the additional yield that investors demand for holding a bond with credit risk over a similar‑maturity, high‑quality government security.

2 As of September 24, 2021, and is subject to change.

-

Additional Disclosure

Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright © 2021, J.P. Morgan Chase & Co. All rights reserved.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. These risks are generally greater for investments in emerging markets. Fixed-income securities are subject to credit risk, liquidity risk, call risk, and interest-rate risk. As interest rates rise, bond prices generally fall. Investments in high-yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities.

The views contained herein are those of the authors as of September 2021 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2021 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.