Choose your location

Portugal

English

Belgium

Denmark

Estonia

Finland

France

Iceland

Ireland

Latvia

Lithuania

Luxembourg

Netherlands

Norway

Portugal

Sweden

United Kingdom

June 2023 / Midyear Market Outlook

Economic Resilience Tested

2023 Midyear Market outlook – Theme 1

Economic reports in the first half of 2023 generally painted a grim picture, with many indicators posting declines similar to those seen heading into past US recessions.

An inverted US Treasury yield curve—with shorter‑term yields higher than longer‑term yields—is one of the warning signs that historically has signaled a downturn, Page notes. At the end of May, the yield on the three‑month Treasury bill was 188 bps higher than the yield on the 10‑year Treasury note—just below the all‑time record set earlier in the month.

But those recession warnings could be misleading, or at least incomplete, Page argues. In many cases, the sharp declines seen in such measures as purchasing managers’ indexes, consumer confidence, and the US money supply have been from the inflated levels reached during the pandemic and its aftermath. “A lot of these indicators are flashing red because we’re still unwinding COVID distortions,” he says.

During the pandemic, Page notes, household savings soared as stimulus measures poured money into consumers’ bank accounts faster than they spent it. Now those balances are coming down. But they remain extremely high by historical standards, and debt service ratios are still low.

In the Fed’s most recent survey of senior bank loan officers, nearly half said they’ve tightened lending standards in the wake of the banking crisis—a level also historically associated with recessions, Page notes. But healthy consumer and corporate finances could mitigate the economic impact of tighter credit. “The most important difference now is that the balance sheets are in better shape,” he says.

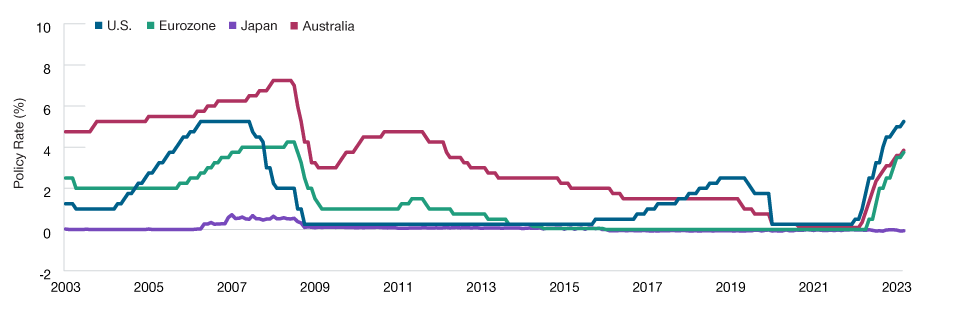

Husain suspects that some financial indicators also could be sending misleading signals about the near‑term direction of central bank policy rates (Figure 2).

Interest Rates May Have to Stay Higher for Longer

(Fig. 2) Central bank policy rates

As of May 31, 2023.

US = Federal Reserve fed funds upper limit. Eurozone = European Central Bank main refinancing rate. Japan = Bank of Japan overnight call rate. Australia = Reserve Bank of Australia official cash rate.

Sources: US Federal Reserve, Statistical Office of the European Communities, Cabinet Office of Japan, Reserve Bank of Australia.

As of late May, Husain notes, interest rate futures markets were forecasting several Fed rate cuts before the end of 2023. He sees that as unlikely, barring a major liquidity crisis and/or an abrupt US plunge into recession.

“I think the market is trying to reconcile two very different scenarios—one where the US economy remains fairly strong and the Fed doesn’t cut rates, and one where things go terribly wrong and the Fed has to cut by several hundred basis points,” Husain explains. “That averages out as what’s priced into the market.”

Near‑term rate cuts are even more unlikely in Europe, Husain adds. In fact, he expects both the European Central Bank (ECB) and the Bank of England to raise rates several times more, despite the economic risks. “I do think the Fed and other central banks will cut rates eventually,” Husain says. “But the timing is tricky. Rates are going to remain higher for longer.”

The Bank of Japan (BoJ) remains an outlier among the key developed central banks, Husain notes, as it still is in quantitative easing mode—including its policy of capping yields on long‑term Japanese government bonds. But this could soon change, he warns.

Arif Husain, CFA

Head of International Fixed Income and Chief Investment Officer

Sébastien Page, CFA

Head of Global Multi‑Asset and Chief Investment Officer

Justin Thomson

Head of International Equity and Chief Investment Officer

Thinking

More Midyear Market Outlook insights

China Market Outlook

A more broad-based recovery after initial reopening, though some bumpiness is expected.

Japan Market Outlook

Macro risks have risen, but the outlook for Japan appears bright.

2023 Midyear Market Outlook

Finding the Signal Through The Noise

Want to know more? Get in touch.

If you have questions or would like more information about T. Rowe Price please contact us.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

EEA – Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L-1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Switzerland - Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

UK - This material is issued and approved by T. Rowe Price International Ltd, Warwick Court, 5 Paternoster Square, London EC4M 7DX which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.