Choose your location

Germany

English

Belgium

Denmark

Estonia

Finland

France

Iceland

Ireland

Latvia

Lithuania

Luxembourg

Netherlands

Norway

Portugal

Sweden

United Kingdom

June 2023 / MidYear Market Outlook

Bonds are Back?

2023 Midyear Market outlook – Theme 2

The sharp rise in bond yields since early 2022 has improved return potential in many fixed income sectors. But an aggressive portfolio shift into longer‑term bonds still appears premature.

“Anyone who universally says that ‘bonds are back’ is being a little too optimistic,” Husain says. “Some bond markets are back. Others may be back in the near future. But I think it’s too sweeping to just say, ‘go out and buy fixed income.’”

Yields on most sovereign bonds and investment‑grade credits still aren’t positive in real (after inflation) terms, Husain notes. And with the US Treasury yield curve close to a record inversion as of late May (Figure 4), investors who trade money market holdings for longer‑term bonds could pay a heavy return penalty.

Negative yield curves make it expensive to extend duration2—especially for investors using borrowed short‑term money to finance their long bond positions, Husain notes. “You end up sacrificing yield on a daily basis.”

Inverted Yield Curve Makes Buying Longer‑Term Bonds Expensive

(Fig. 4) Treasury Yield Curve (10‑Year Minus 3‑Month Constant Maturity)

As of May 31, 2023.

Source: Federal Reserve Bank of St. Louis.

Under these conditions, aggressively extending duration in the US fixed income market amounts to a bet that a recession is near, Husain argues. “You’re saying, ‘I think the Fed will cut rates soon, and probably in a very quick way.’ I’m not sure we can say that, at least not yet.”

But Page thinks a modest increase in duration could be prudent for investors seeking to hedge against that very scenario—the sudden onset of a US recession followed by rapid Fed rate cuts.

T. Rowe Price’s Asset Allocation Committee, Page notes, has modestly extended duration in its multi‑asset portfolios—both to guard against a growth shock and to potentially enhance returns if one does push yields sharply lower. “When you look at our tactical positions, we’re playing both defense and offense.”

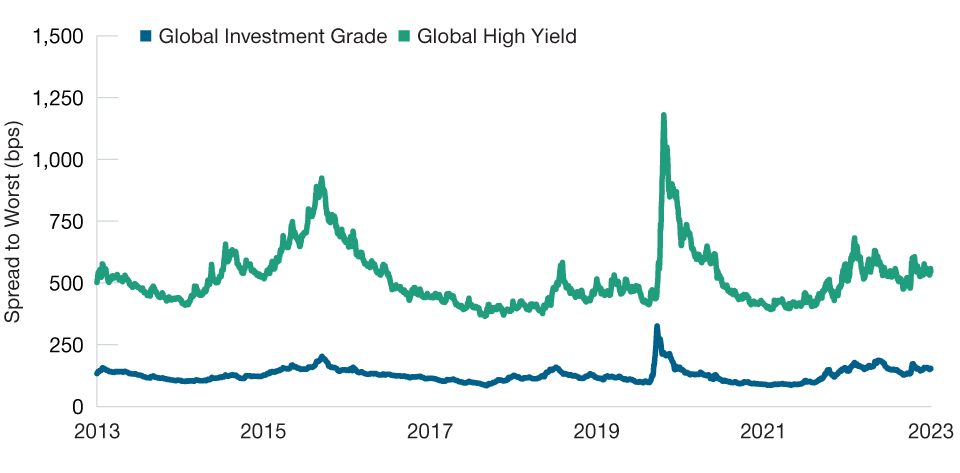

High on High Yield

The rise in yields may have created more significant opportunities in corporate credit, Husain says. Yields in the 8%–10% range and credit spreads close to their 10‑year average (Figure 5) make the global high yield market attractive in any scenario short of a deep global recession, he argues.

Global Credit Sectors Offer Opportunities

(Fig. 5) Investment‑grade and high yield spreads, in basis points

As of May 31, 2023. Past performance is not a reliable indicator of future performance. Global high yield = J.P. Morgan Global High Yield Index. Global investment grade = Bloomberg Global Aggregate Corporate Index. Spreads versus sovereign bonds with similar duration.

Sources: J.P. Morgan Chase (see Additional Disclosures), Bloomberg Finance L.P. T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

Slower economic growth and higher rates are likely to push default rates up gradually over the balance of 2023 and into 2024, Husain says. But with corporate balance sheets, on average, still featuring low leverage and ample debt service coverage, default risks appear moderate, he argues.

Based on their credit research, Page adds, T. Rowe Price analysts as of late May were forecasting a US high yield default rate of about 3% over the next 12 months, roughly in line with the longer‑term historical average.

“We don’t see default rates getting anywhere close to eroding the extra yield premium, relative to investment‑grade bonds, that you can get in high yield right now,” Husain says.

Bottom‑up research and skilled security selection will be critical to managing default risk, Page cautions. “Skilled active managers know how to differentiate between healthy versus true junk balance sheets.” This, he contends, can help investors avoid “zombies”—companies that are still technically in business but almost certainly are headed toward bankruptcy.

1 Duration is a measure of the interest rate risk on fixed income securities. Generally, bonds with longer maturities also have longer duration.

Arif Husain, CFA

Head of International Fixed Income and Chief Investment Officer

Sébastien Page, CFA

Head of Global Multi‑Asset and Chief Investment Officer

Justin Thomson

Head of International Equity and Chief Investment Officer

Thinking

More Midyear Market Outlook insights

Economic Resilience Tested

2023 Midyear Market Outlook – Theme 1

Focus on Earnings

2023 Midyear Market Outlook – Theme 3

2023 Midyear Market Outlook

Finding the Signal Through The Noise

Sign up to receive our Fixed Income insights

Want to know more? Get in touch.

If you have questions or would like more information about T. Rowe Price please contact us.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

EEA – Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L-1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Switzerland - Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

UK - This material is issued and approved by T. Rowe Price International Ltd, Warwick Court, 5 Paternoster Square, London EC4M 7DX which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.