ADDITIONAL SURVEY RESULTS:

COVERING COLLEGE COSTS

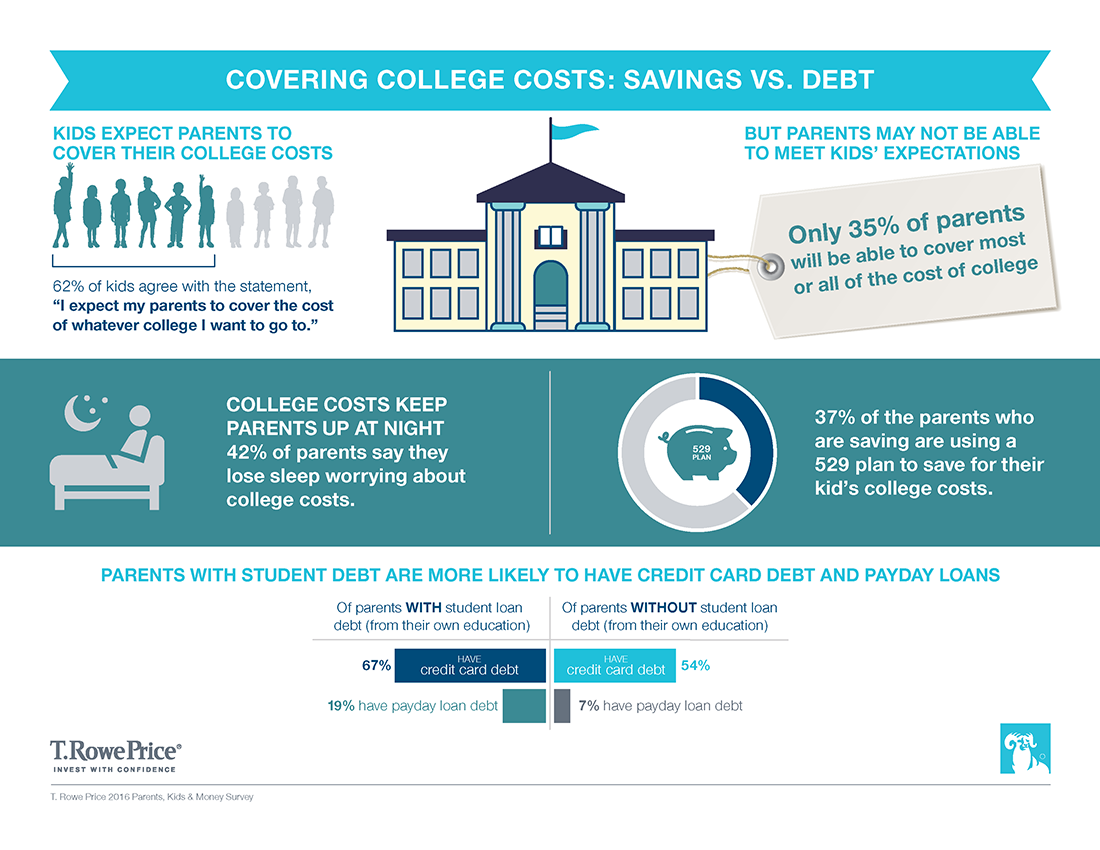

- Kids expect parents to cover their college costs: 62% of kids agree with the statement, “I expect my parents to cover the cost of whatever college I want to go to.”

- But parents may not be able to meet kids’ expectations: Only 35% of parents will be able to cover at least most of college costs, including 12% of parents who indicated they will be able to pay the entire cost of college.

- Some kids think their parents are saving for their college when they are not: 67% of kids say their parents are saving for their college. But, nearly a quarter of those (23%) have parents who said that they actually are not saving for their college.

- And many parents feel guilty: 63% of parents agree with the statement, “I feel guilty that I won’t be able to pay more for their college.”

- College costs keep more parents up at night today: 42% of parents agree with the statement, “I lose sleep worrying about college costs,” up significantly from 2014 when the same question was asked and 28% of parents indicated that they lose sleep over college costs.2

- Parents are willing to work more to cover college costs: 76% of parents would be willing to delay their retirement and 68% would be willing to get a second or part-time job to pay for kids’ college education.

- And parents tend to underestimate college costs: While the total cost of a four-year education at an in-state university is currently about $80,000 on average, according to The College Board1, only 35% of parents think that the total cost of a four-year education at an in-state university is $80,000 or more.

STUDENT LOAN BURDEN

- More than a quarter of parents have student loans: 28% of parents are paying back student loans, either for their own education (20%) or their kids’ education (12%). A minority of parents (5%) have both student loan debt for their own education and their kids’.

- Parents with student debt are more likely to have credit card debt and payday loans: Parents paying off student loans from their own education are significantly more likely to have credit card debt (67% vs. 54%) and payday loans (19% vs. 7%). And parents paying back loans for their kids’ education are even more likely to have credit card debt (75% vs. 54%) and payday loan debt (38% vs. 5%).

- Some parents are willing to take on considerable student loan debt: 57% of parents are willing to take on $25,000 or more in debt to pay for their kids’ college education, with 19% willing to borrow $100,000 or more.

- And they are willing to let their kids take student loans: Nearly half (47%) are willing to let their kids borrow $25,000 or more, with 14% willing to let their kids take out $100,000 or more in student debt.

- Parents who have student debt are more willing to take on higher levels of debt: Parents who are paying back their own student loans are more willing to borrow $100,000 or more themselves to pay for their kids’ college (24% vs. 18%).

COLLEGE SAVINGS MISCONCEPTIONS AND BENEFITS:

- More parents have money saved for their kids’ college than their own retirement: While 58% of parents said they had money saved for their kids’ college education, only 54% indicated they had money saved for their retirement.

- Parents sometimes use the wrong account to save for college: 43% of parents are using a regular savings account to save for their kids’ college and 27% are using a retirement account (401(k) or IRA). 37% are saving appropriately by using 529 college savings account.

- Millennials are less likely to use 529 college savings accounts: Nearly half as many Millennials are saving for their kids’ college in a 529 account (22%) compared with Gen Xer (42%) and Baby Boomer (42%) parents.

- Parents using 529 accounts are less likely to spend college savings on other things: 38% of parents saving for their kid’s college in a 529 account have used their college savings to pay for other expenses, compared to 49% of parents who are not using a 529 account to save for college. Common reasons for taking money out of college savings including paying for vacation (13%), taxes (13%), health care (12%), home repair or renovation (12%), and paying off debt (12%).

- Most parents recognize the need to start saving for college early: 68% of parents think they should start saving for their kids’ college education when their kids are 10 or younger, including 28% of parents that think kids should be 1 years old when they start saving for college. However, nearly one-fifth (19%) of parents think that they should wait until their kids are teenagers to start saving for their college education.

1National Average Cost Data: ©2016 The College Board, “Trends in College Pricing 2015.”

22014 T. Rowe Price Parents, Kids & Money Survey

Please note that a 529 plan’s disclosure document includes investment objectives, risks, fees, expenses, and other information that you should read and consider carefully before investing. You should compare any 529 college savings plan with the 529 college savings plan offered by your home state or your beneficiary’s home state. Before investing, consider any state tax or other benefits that are only available for investments in the home state’s plan.

ABOUT THE SURVEY

The eighth annual T. Rowe Price Parents, Kids & Money Survey, conducted by MetrixLab, Inc., aimed to understand the basic financial knowledge, attitudes, and behaviors of both parents of kids ages eight to 14 and their kids ages 8 to 14. The survey was fielded from February 4, 2016 through February 11, 2016, with a sample size of 1,086 parents and 1,086 kids ages 8 to 14. The margin of error is +/- 3 percentage points. All statistical testing done among subgroups (e.g., boys versus girls) is conducted at the 95% confidence level. Reporting includes only findings that are statistically significant at this level.

ABOUT T. ROWE PRICE

Founded in 1937, Baltimore-based T. Rowe Price Group, Inc. (troweprice.com) is a global investment management organization with $776.6 billion in assets under management as of June 30, 2016. The organization provides a broad array of mutual funds, subadvisory services, and separate account management for individual and institutional investors, retirement plans, and financial intermediaries. The company also offers a variety of sophisticated investment planning and guidance tools. T. Rowe Price's disciplined, risk-aware investment approach focuses on diversification, style consistency, and fundamental research. For more information, visit troweprice.com or our Twitter, YouTube, LinkedIn, and Facebook sites.